The Impact of the CFPB’s New Regulations on Payment Apps and Digital Wallets

Latinia

•10 de December de 2024•6 min read

The financial sector is undergoing a profound transformation driven by digitalization and the rise of new technologies. Among these, digital wallets like Apple Pay, Google Pay, and PayPal have taken center stage, offering consumers fast and convenient alternatives for transactions. This phenomenon has redefined how people manage their money, partially displacing traditional payment methods.

Furthermore, the exponential growth of e-commerce and digital services has accelerated the adoption of these platforms, creating an increasingly interconnected financial ecosystem. However, while banks have long operated under strict regulatory frameworks,digital payment platforms in the United States had largely remained outside these regulations—until now.

The Rise of Digital Wallets

Digital wallets enable functionalities such as contactless payments in physical stores using NFC technology, instant transfers between users, and the storage of financial information like credit and debit cards, and even cryptocurrencies. Additionally, they have played a crucial role in financial inclusion, allowing unbanked individuals to access basic services through mobile devices.

This impact has driven exponential growth in their adoption:

Transaction Volume: Over 13 billion transactions are processed annually through these platforms.

User Growth: Global penetration of digital wallets is estimated to exceed 40% among smartphone users.

Generational Preference: Millennials and Gen Z are the largest adopters, driven by their need for speed and convenience in transactions.

New Regulations in the U.S. Financial Sector

Regulation plays a crucial role in maintaining a secure, transparent, and accessible financial system. With the growing use of payment apps and digital wallets, the need for proper oversight has intensified. These platforms handle large volumes of transactions and sensitive data, making them critical touchpoints within the financial system.

In this context, the U.S. Consumer Financial Protection Bureau (CFPB) has introduced a regulation extending oversight to companies handling more than 50 million transactions annually, limited to operations in U.S. dollars. Building on previous CFPB actions, this regulation addresses risks such as the lack of federal insurance for funds stored in payment apps and the use of behavioral targeting in financial products. Scheduled to take effect 30 days after publication, the regulation aims to align fintech oversight with that of traditional banks, protecting consumers and fostering fairer competition.

The new regulation seeks to address three key challenges posed by payment apps:

Data Privacy and Usage: Digital wallets collect and manage vast amounts of personal and financial data, raising concerns about transparency and the ethical handling of this information.

Errors and Fraud: The rise of digital transactions has increased the risk of operational errors and fraudulent activities, particularly on less-regulated platforms.

Competitive Imbalance: Fintech and big tech companies operating digital wallets have grown rapidly, challenging traditional banking institutions that historically operate under stricter regulations.

Key Points of the New Regulation

Consumer Protection

The regulation aims to ensure that users of payment apps have access to clear and efficient solutions to address transaction errors or fraud. Additionally, these companies are expected to offer users the option to opt out of certain data collection practices, thereby providing greater autonomy and control over personal information.

Error and Fraud Prevention

A cornerstone of the regulation is the requirement for platforms to effectively investigate and resolve errors reported by consumers. This includes establishing clearer processes for dispute resolution and ensuring timely and fair outcomes.

Data Management Transparency

The regulations mandate digital wallets to provide clear information on how user data is utilized and shared. The goal is to reduce the risk of misuse or unauthorized access to sensitive information.

Competitive Fairness

By bringing fintech companies under a regulatory framework similar to that of traditional banks, the regulation seeks to level the playing field, promoting fair competition without compromising consumer security or trust.

These regulations represent a milestone in the financial sector, treating digital wallets not merely as technological services but as essential players in the global financial infrastructure

Impact of Digital Wallets on Traditional Banking

Digital wallets have reshaped the financial system, significantly impacting traditional banks in several key areas:

Reduced Use of Banking Platforms: Users increasingly prefer to integrate their bank cards into wallets like Apple Pay and Google Pay, decreasing reliance on banking apps and diverting transaction revenue to these platforms.

Weakened Customer-Bank Relationship: Wallets act as intermediaries, reducing direct interactions between users and their banks, which weakens the historic connection between the two parties.

Competition in Financial Services: Platforms like PayPal and Cash App have expanded their offerings to include products such as loans and insurance, directly competing with banks in critical areas.

New Customer Expectations: Generations like Millennials and Gen Z demand fast, frictionless services, pushing banks to invest in technology to modernize their user experience.

Challenges for Banks: Customer Acquisition and Retention in a Digital Landscape

Digital wallets pose significant challenges for traditional financial institutions, which must adapt to an ever-changing market:

Competition for Customer Attention: Banks must develop apps and services that match or surpass the user experience offered by digital wallets.

Loss of Transaction Revenue: By acting as intermediaries, digital wallets capture a share of transaction fees that previously belonged exclusively to banks.

Shared Regulatory Risks: New regulations that align digital wallets with banks also increase compliance expectations for both, requiring greater investments in technology and security.

Despite these challenges, financial institutions hold a key advantage: customers’ historical trust. To remain relevant, banks must prioritize innovation, collaboration with fintechs, and the creation of personalized experiences that leverage their expertise and stability.

Banking Sector’s Response to Digital Transformation

The digital transformation has compelled traditional banks to adapt swiftly, integrating digital wallets and payment apps as essential components of their services. This integration addresses the need to deliver faster, more user-friendly experiences while competing with fintechs and major tech platforms.

Banks have adopted various strategies to achieve this transformation:

Collaboration with External Platforms: Banks have partnered with services like Apple Pay, Google Pay, and Samsung Pay, enabling customers to link their accounts and cards for mobile and contactless payments, enhancing service accessibility.

Development of Proprietary Wallets: Some financial institutions have launched their own payment apps, offering features such as instant transfers, in-store payments, and financial management directly from their mobile platforms.

Technological Modernization: Banks have invested in upgrading their infrastructure to ensure compatibility with emerging payment technologies and to provide faster, more secure, and seamless transactions.

In this context, the integration of Latinia’s solutionssignificantly enhances banks’ ability to manage communications, including those related to wallets and payment apps.

For instance, Latinia’s Next Best Action (NBA) tool allows banks to identify the best moment to send personalized notifications to customers based on historical and transactional data. For example, a customer who does not use the bank’s digital payment options might receive a mobile notification while making a purchase with their card: “Remember, you can also use Bank X’s digital payments for a faster and more convenient experience.”

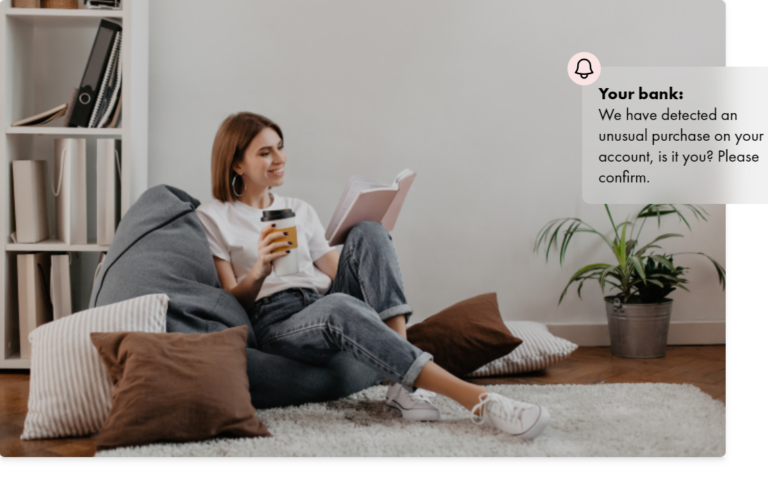

Additionally, Latinia’s Critical Events Gateway facilitates the detection of suspicious activities, such as unusual transaction attempts. In such cases, the system immediately notifies the customer, enabling quick action and reinforcing security and trust in the bank’s services.

The Importance of Regulatory Adaptation in Today’s Landscape

The implementation of new regulations in the financial sector marks a crucial step in ensuring that digital payment platforms, such as wallets, operate within a framework of security, transparency, and fair competition. With their growing adoption and central role in consumers’ financial lives, it is essential for tech companies and financial institutions to adapt to a regulatory environment that protects users while fostering innovation.

For digital wallets, adopting these new regulations presents a significant challenge, requiring greater investments in technology and regulatory compliance. Many platforms will need to adjust their internal processes to ensure transparency in data management and effective resolution of errors and fraud. On the other hand, these regulations also present an opportunity to build consumer trust and establish themselves as reliable players within the financial ecosystem.

The future of the banking sector is closely tied to the development of digital technologies and the integration of services like wallets. Traditional financial institutions must recognize that digital wallets are not just competitors but also opportunities to reinvent their services and reach new customer segments.

For traditional banks, the new regulations level the competitive playing field with fintech and big tech companies, reinforcing fairness in the market. However, by removing the historical trust advantage derived from regulatory compliance, banks will need to double down on digitalization and user experience improvements to remain competitive.

Success lies in the ability of banks to adapt, collaborate with fintechs, and leverage digital tools to deliver more agile and personalized experiences. They must also proactively meet new regulatory requirements, ensuring their continued relevance in an increasingly digitalized world.

The key will be finding a balance between regulation and innovation, enabling the banking sector to continue evolving to meet the needs of future consumers while ensuring the security, transparency, and trust that users expect.

Discover how Latinia can transform your bank’s customer interactions. Contact us today for more information or to request a demo of our powerful real-time messaging solutions.

The financial sector is undergoing a profound transformation driven by digitalization and the rise of new technologies. Among these, digital wallets like Apple Pay, Google Pay, and PayPal have taken…

The financial sector is undergoing a profound transformation driven by digitalization and the rise of new technologies. Among these, digital wallets like Apple Pay, Google Pay, and PayPal have taken…

The financial sector is undergoing a profound transformation driven by digitalization and the rise of new technologies. Among these, digital wallets like Apple Pay, Google Pay, and PayPal have taken…

The financial sector is undergoing a profound transformation driven by digitalization and the rise of new technologies. Among these, digital wallets like Apple Pay, Google Pay, and PayPal have taken…

The financial sector is undergoing a profound transformation driven by digitalization and the rise of new technologies. Among these, digital wallets like Apple Pay, Google Pay, and PayPal have taken…

The financial sector is undergoing a profound transformation driven by digitalization and the rise of new technologies. Among these, digital wallets like Apple Pay, Google Pay, and PayPal have taken…

The financial sector is undergoing a profound transformation driven by digitalization and the rise of new technologies. Among these, digital wallets like Apple Pay, Google Pay, and PayPal have taken…

The financial sector is undergoing a profound transformation driven by digitalization and the rise of new technologies. Among these, digital wallets like Apple Pay, Google Pay, and PayPal have taken…

The financial sector is undergoing a profound transformation driven by digitalization and the rise of new technologies. Among these, digital wallets like Apple Pay, Google Pay, and PayPal have taken…

The financial sector is undergoing a profound transformation driven by digitalization and the rise of new technologies. Among these, digital wallets like Apple Pay, Google Pay, and PayPal have taken…

The financial sector is undergoing a profound transformation driven by digitalization and the rise of new technologies. Among these, digital wallets like Apple Pay, Google Pay, and PayPal have taken…

The financial sector is undergoing a profound transformation driven by digitalization and the rise of new technologies. Among these, digital wallets like Apple Pay, Google Pay, and PayPal have taken…

Para ofrecer las mejores experiencias, utilizamos tecnologías como las cookies para almacenar y/o acceder a la información del dispositivo. El consentimiento de estas tecnologías nos permitirá procesar datos como el comportamiento de navegación o las identificaciones únicas en este sitio. No consentir o retirar el consentimiento, puede afectar negativamente a ciertas características y funciones.

Funcional

Always active

El almacenamiento o acceso técnico es estrictamente necesario para el propósito legítimo de permitir el uso de un servicio específico explícitamente solicitado por el abonado o usuario, o con el único propósito de llevar a cabo la transmisión de una comunicación a través de una red de comunicaciones electrónicas.

Preferencias

El almacenamiento o acceso técnico es necesario para la finalidad legítima de almacenar preferencias no solicitadas por el abonado o usuario.

Estadísticas

El almacenamiento o acceso técnico que es utilizado exclusivamente con fines estadísticos.El almacenamiento o acceso técnico que se utiliza exclusivamente con fines estadísticos anónimos. Sin un requerimiento, el cumplimiento voluntario por parte de tu proveedor de servicios de Internet, o los registros adicionales de un tercero, la información almacenada o recuperada sólo para este propósito no se puede utilizar para identificarte.

Marketing

El almacenamiento o acceso técnico es necesario para crear perfiles de usuario para enviar publicidad, o para rastrear al usuario en una web o en varias web con fines de marketing similares.