Senior Banking in the Digital Era

Bank branches continue to play a key role in customer service, but long wait times remain a challenge for both financial institutions and their clients. Despite the rise of digital banking, many…

Read More

Latinia

Latinia

Bank branches continue to play a key role in customer service, but long wait times remain a challenge for both financial institutions and their clients. Despite the rise of digital banking, many customers still visit branches for specific transactions, leading to crowding and a less-than-ideal experience. Reducing branch traffic not only improves operational efficiency for banks but also enhances the customer experience, allowing them to resolve their needs more quickly and conveniently. In this article, we’ll explore the current state of bank branches, the main reasons customers still visit them, and the strategies banks can implement to reduce wait times.

Bank branches have been shrinking as technology and digital banking have evolved, making it easier for customers to access financial services without visiting a physical location. Most clients can now manage their accounts, make payments, and apply for financial products from their mobile devices or computers, changing the way they interact with their banks.

This shift has had a significant impact on the number of bank branches:

Despite branch closures, this does not mean in-person banking demand has disappeared. Fewer branches result in more customers concentrated in the remaining locations, which can lead to longer wait times and a less satisfying experience. This trend also affects other service channels, such as bank call centers. Reducing in-branch traffic must go hand in hand with strategies to optimize other touchpoints, preventing overload in customer service centers.

According to the American Bankers Association (ABA), 55% of customers prefer mobile apps for banking transactions, while 22% use online banking. Only 8% still visit a branch, while the remaining customers use ATMs (5%), phone banking (4%), or even postal mail (1%).

Although branch visits are becoming less frequent, they remain necessary for certain transactions. Banks must find ways to reduce foot traffic without compromising service quality. The key lies in understanding why customers still visit branches and what they need, providing them with the right tools to manage their banking needs independently.

Although many everyday transactions can be handled through mobile apps or online platforms, there are situations where customers prefer—or need—to visit a branch in person.

According to the latest studies by Rivel on branch demand, there are four main reasons why customers choose in-person service over digital channels:

The goal is not only to speed up in-branch service but also to offer alternatives that allow customers to complete transactions without having to visit a branch. This involves optimizing resource allocation, enhancing self-service options, and leveraging real-time technology to guide customers toward more efficient channels based on their needs. Below are some key strategies to reduce branch traffic without compromising service quality.

One of the main causes of congestion in bank branches is inefficient customer flow management. Walk-in service often leads to crowding during peak hours and longer wait times, negatively impacting the customer experience. To address this, banks can implement appointment scheduling and queue management systems to better distribute branch traffic.

Digital appointment tools allow customers to book a visit based on their availability, reducing the need to wait in person. Additionally, assigning queue numbers through apps, SMS messages, or real-time notifications can help streamline in-branch service and prevent unnecessary overcrowding.

Many in-branch transactions could be completed without direct interaction with a banker, as long as the right tools are available. Installing self-service kiosks within bank branches allows customers to perform transactions such as transfers, data updates, balance inquiries, or document printing without waiting in line for a representative.

Additionally, combining these kiosks with digital assistance—such as in-branch chatbots—helps customers resolve questions without needing an employee’s help. This not only speeds up service but also allows bank staff to focus on more complex transactions that require personalized attention.

Customers who visit branches for transactions that can be done quickly online often do so due to a lack of awareness about alternatives, low trust in digital channels, or difficulty adapting to technology. This is especially common among older adults who, despite the benefits of mobile banking, often face barriers due to unfamiliarity with digital devices or fear of making mistakes.

To reduce in-branch traffic, banks must actively promote the use of their mobile apps and online platforms, making it easier for customers to transition to self-service banking.

An effective strategy is customer education through tutorials, personalized assistance, and communication campaigns that explain how to safely complete transactions online. Additionally, gamification and incentives—such as discounts or exclusive benefits for online banking users—can help increase adoption.

Branch staff also play a key role in this process. If employees actively encourage customers to use digital banking by explaining how they can meet their needs without visiting a branch, it will be easier to reduce reliance on in-person service.

In many cases, customers start a transaction online but, after encountering difficulties or being unable to complete it, end up visiting a branch for assistance. This issue can be avoided if banks optimize their omnichannel strategy, ensuring a seamless and consistent experience across all touchpoints.

To achieve this, customer information must be synchronized across all channels. If a customer starts a loan application online, they should be able to continue it smoothly over the phone with an advisor or, if they visit a branch, receive assistance without having to start the process from scratch. Similarly, implementing advanced chatbots and virtual assistants with access to customer history can help answer questions without requiring a branch visit.

Another key factor is personalized interactions. If banks can anticipate customer needs and guide them to the most efficient channel for each type of transaction, they can reduce unnecessary branch visits and improve the overall customer experience.

In a world where immediacy is key, banks cannot simply react to customer issues—they must anticipate them. Real-time technology enables financial institutions to deliver a faster, more efficient experience, reducing the need for customers to visit a branch to resolve their problems.

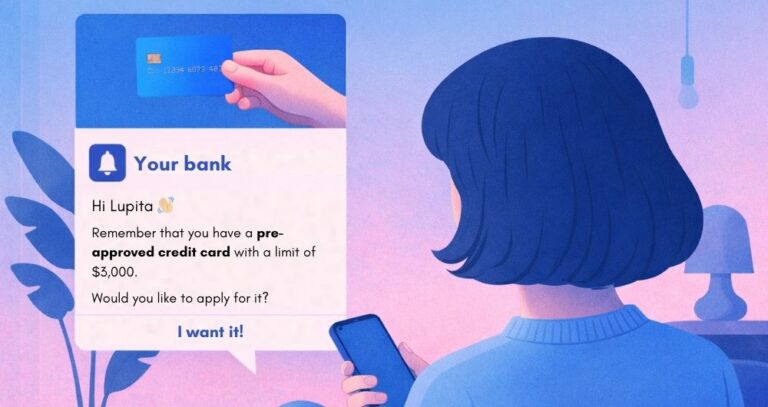

This is where Latinia makes a difference. By filtering and analyzing transactional events in real time, our solutions help banks shift from reactive to proactive customer service, providing relevant information at the right moment and preventing unnecessary branch visits.

For example, when a customer tries to make a payment and their card is declined due to reaching their credit limit, they typically contact phone support or visit a branch to understand what happened. However, with Latinia’s technology, the bank can instantly send a notification explaining the situation and offering a solution, such as increasing the credit limit or making a payment to free up available funds.

This not only prevents a branch visit but also enhances the overall customer experience.

Latinia’s Next Best Action (NBA) real-time decision engine is key to this transformation. It doesn’t just analyze data—it contextualizes it to deliver personalized notifications and solutions.

Additionally, its seamless integration with a bank’s existing systems ensures a smooth transition to a proactive service model without disrupting current processes.

You can also turn your bank branch into a hub of efficiency and customer satisfaction. Contact us today and let Latinia guide you toward a future of seamless, proactive banking communications.

Contact