How to tackle regulatory changes and recent bank mergers with a resilient tech architecture.

Are banks equipped with a robust and adaptable tech architecture that allows them to successfully face the challenges posed by recent mergers and evolving regional and international regulations?

In 2025, banking resilience in Latin America and the European Union is being put to the test by increasing consolidation and mergers, within a global landscape marked by regulatory divergence: while key Anglo-Saxon markets such as the US and the UK are easing certain rules (including Basel III.1 and other protective mechanisms), others are moving toward stricter and more complex frameworks. This disparity adds uncertainty and demands that banks rely on solid, adaptable technological architectures to meet new requirements and protect both financial and reputational stability.

In this context, technological dependence and the strength of the infrastructure supporting critical processes—such as notifying clients of important events—have become key factors in safeguarding the financial and reputational stability of banks across the region.

Global context: regulatory divergence and banking consolidation

In 2025, both the United Kingdom and the United States are easing regulations introduced after the 2008 financial crisis, including delaying and softening elements of the Basel 3.1 framework and other protective mechanisms (like ring-fencing), with the stated goal of boosting competitiveness and economic growth.

UK authorities, for example, have announced new capital rules to be implemented in 2027 and 2028 aimed at striking a balance between stability and proactive banking expansion, offering relief especially to mid-sized and smaller banks:

Implementation of most of Basel 3.1 starting in 2027, with the new internal model approach for market risk postponed to 2028.

Introduction of the Strong and Simple regime, with more proportional capital requirements for smaller institutions.

Revision of MREL thresholds and improved access to internal models for mid-sized banks to foster competition.

At the same time, the US and the UK have strengthened their regulatory cooperation through the Financial Regulatory Working Group, focusing on maintaining strong standards for global financial stability while promoting a more growth-friendly system.

Meanwhile, Latin America and the European Union are experiencing a clear wave of banking consolidation.

The gradual withdrawal of major multinationals from Latin America—such as Citibank and Scotiabank exiting several countries in the region—has encouraged mergers among local players and the emergence of new interregional “mega-franchises” (like the merger between Bicecorp and Banco Security, or Davivienda with Scotiabank).

Mexico, Chile, Colombia, and Central American countries are at the center of this trend, with large institutions looking to expand through acquisitions and smaller banks being forced to merge or be absorbed to survive increasingly demanding regulatory and technological requirements.

In the European Union, public takeover bids have surged across the continent over the past 12 months. The European Central Bank strongly supports the creation of continental-scale banking giants capable of competing with US firms, but in practice, most deals remain within national borders.

Global outlook on mergers and acquisitions in Latin America and Europe

In Latin America, according to KPMG, the financial sector ranks among the top three most attractive for mergers and acquisitions over the next two years—second only to technology. Interest is especially high in Mexico and Brazil, the region’s largest and relatively most stable markets, though Costa Rica is emerging as a new destination for upcoming deals.

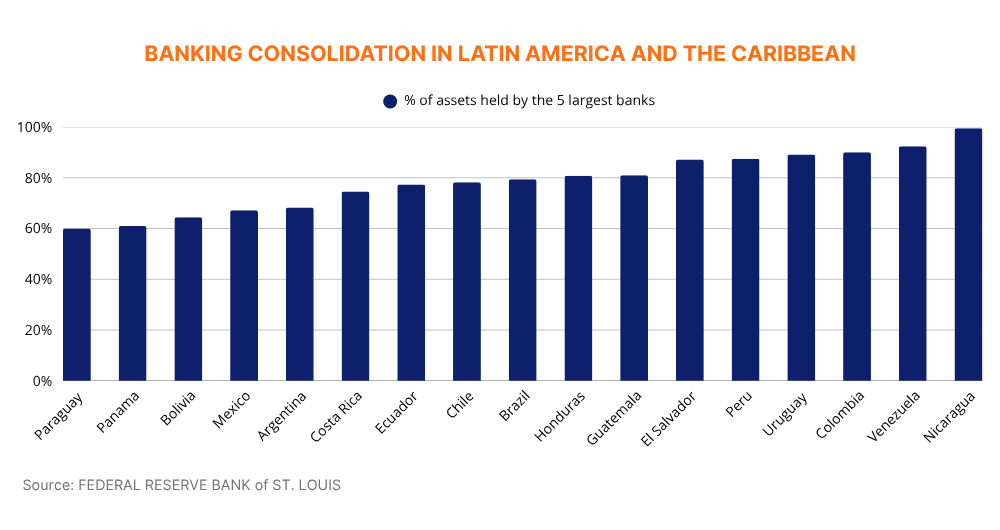

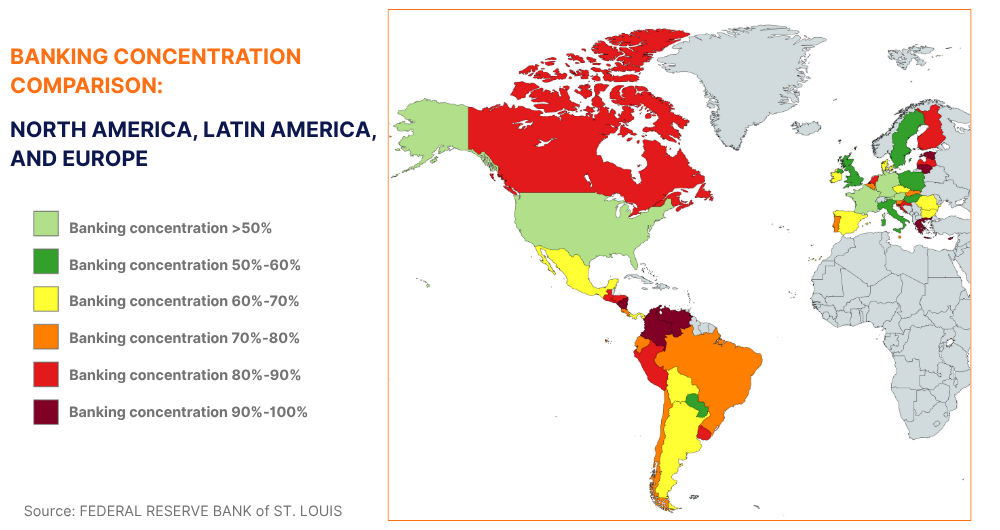

In terms of banking concentration, data from FRED shows a diverse landscape across the region: Venezuela has the highest banking concentration (92.4%), followed by Colombia (90.1%), Uruguay (89.2%), Peru (87.5%), and El Salvador (87.2%), while Mexico (67.2%) and Argentina (68.3%) show the lowest concentration. Overall, the region displays medium to high levels of banking concentration, with notable differences between countries.

In the European Union, according to data from a report on M&A activity in Europe, banking concentration has been steadily increasing over the past two decades. The European Central Bank reports that the concentration ratio (CR-5) now exceeds 65% in several eurozone countries, and the number of active institutions has been consistently declining since 2008—particularly in markets like Germany and Italy, where the highest volume of deals is recorded. Although most mergers are domestic (around 80% of the total), the result is a banking system dominated by a small group of large institutions with an increasing share of sector assets.

In Spain, for example, 68.5% of banking assets are held by the five largest banks, and that figure is expected to exceed 70% if further integrations occur. Similar trends are visible in France and Italy, where the top five banks control roughly 45–50% of national assets, reflecting a common pattern of reduced market competition across Europe.

Resilience under pressure: risks of banking concentration

The rise in banking concentration means fewer institutions are managing larger volumes of assets and customers. From a systemic stability perspective, this increases the risk that a single technological failure, cyberattack, or operational issue could have a ripple effect on the economy—especially when it involves regionally significant institutions.

In markets where regulation is becoming more relaxed, supervisory control weakens, raising the risk of crises. In regions with stricter rules, the pressure on mid-sized and smaller banks to adapt technologically is much higher. On top of that, increasing digitalization and the adoption of new technologies are making banks more dependent on their tech infrastructure and the strength of critical processes—such as managing critical notifications that alert customers to fraud, suspicious activity, or operational disruptions.

Rethinking banking resilience: the case of critical notifications

Resilience is no longer just about strong balance sheets or capital coverage—it now extends to technological infrastructure. Today, the continuity and reliability of critical notifications (fraud alerts, account blocks, urgent authorizations, etc.) are essential to protecting both customers and banks in the face of incidents, attacks, or major disruptions.

Any interruption in these flows can lead to significant financial losses, reputational damage, and—at scale—serious impacts on trust and overall sector stability.

Resilient architectures: technological shielding

Recent experience shows that banking consolidation processes often lead to abrupt reorganizations of infrastructure, communication channels, and customer bases. This increases operational risk: a single interruption or system failure can affect millions of users.

In this context, resilience-based architectures—such as those offered by Latinia—play a critical role by being designed for precisely these scenarios:

Continuity of banking notifications: Latinia ensures that critical messages (e.g., fraud alerts, unusual transactions, account blocks) reach the end user even under extreme conditions, thanks to redundancy mechanisms, load balancing across providers and channels, and fast-recovery protocols in the event of incidents.

Delivery quality and efficiency: The platform’s 24/7 monitoring enables the early detection or anticipation of channel failures, automatically switching to alternative routes like SMS, push, email, or banking apps. This ensures the highest possible delivery success rate, even when core systems are under pressure.

Full traceability and visibility: Every notification is logged at every stage, allowing technical teams to audit, resolve issues, and provide evidence to regulators regarding proper handling of critical alerts.

Smart prioritization management: Latinia’s platform distinguishes between critical operational messages and those of a commercial or informational nature, assigning priority resources and channels to the former—an essential capability during periods of heavy load following a merger.

Is it time to rethink banking resilience?

Absolutely. In 2025, banking resilience is facing a critical challenge due to the growing concentration of institutions, recent mergers among major local and regional players, and a more relaxed regulatory environment driven by global benchmarks like the UK and the US.

This combination is redefining the rules of the game and further exposing banks’ technological dependence. In this context, the strength of their critical infrastructure—particularly their ability to ensure the continuity and quality of customer notifications—becomes a key factor for financial stability, institutional reputation, and consumer protection.

The intersection of accelerated digitalization, the rise of new fintech players, and the consolidation of large banks is testing resilience like never before. Banks that fail to reinforce their critical notification platforms risk falling short of regulatory requirements, losing customer trust, or—at worst—triggering systemic crises that are difficult to contain.

In 2025, rethinking resilience means going beyond regulatory capital and strengthening the operational core with technology solutions like the resilient notification architecture provided by Latinia.

This platform turns the continuity, traceability, and prioritization of critical alerts into a true “digital life insurance” for post-merger banks, enabling them to operate securely and nimbly in an increasingly complex systemic environment. In doing so, institutions will be better prepared to navigate the ongoing wave of banking integration while reinforcing their ability to prevent disruptions, protect customers, and preserve the stability of the regional financial system.

Want to strengthen the resilience of your banking infrastructure? Learn more about our resilience features, talk to a Latinia expert, or visit our website for more details.

How to tackle regulatory changes and recent bank mergers with a resilient tech architecture.

Are banks equipped with a robust and adaptable tech architecture that allows them to successfully face…

How to tackle regulatory changes and recent bank mergers with a resilient tech architecture.

Are banks equipped with a robust and adaptable tech architecture that allows them to successfully face…

How to tackle regulatory changes and recent bank mergers with a resilient tech architecture.

Are banks equipped with a robust and adaptable tech architecture that allows them to successfully face…

How to tackle regulatory changes and recent bank mergers with a resilient tech architecture.

Are banks equipped with a robust and adaptable tech architecture that allows them to successfully face…

How to tackle regulatory changes and recent bank mergers with a resilient tech architecture.

Are banks equipped with a robust and adaptable tech architecture that allows them to successfully face…

How to tackle regulatory changes and recent bank mergers with a resilient tech architecture.

Are banks equipped with a robust and adaptable tech architecture that allows them to successfully face…

How to tackle regulatory changes and recent bank mergers with a resilient tech architecture.

Are banks equipped with a robust and adaptable tech architecture that allows them to successfully face…

How to tackle regulatory changes and recent bank mergers with a resilient tech architecture.

Are banks equipped with a robust and adaptable tech architecture that allows them to successfully face…

How to tackle regulatory changes and recent bank mergers with a resilient tech architecture.

Are banks equipped with a robust and adaptable tech architecture that allows them to successfully face…

How to tackle regulatory changes and recent bank mergers with a resilient tech architecture.

Are banks equipped with a robust and adaptable tech architecture that allows them to successfully face…

How to tackle regulatory changes and recent bank mergers with a resilient tech architecture.

Are banks equipped with a robust and adaptable tech architecture that allows them to successfully face…

How to tackle regulatory changes and recent bank mergers with a resilient tech architecture.

Are banks equipped with a robust and adaptable tech architecture that allows them to successfully face…

Para ofrecer las mejores experiencias, utilizamos tecnologías como las cookies para almacenar y/o acceder a la información del dispositivo. El consentimiento de estas tecnologías nos permitirá procesar datos como el comportamiento de navegación o las identificaciones únicas en este sitio. No consentir o retirar el consentimiento, puede afectar negativamente a ciertas características y funciones.

Funcional

Always active

El almacenamiento o acceso técnico es estrictamente necesario para el propósito legítimo de permitir el uso de un servicio específico explícitamente solicitado por el abonado o usuario, o con el único propósito de llevar a cabo la transmisión de una comunicación a través de una red de comunicaciones electrónicas.

Preferencias

El almacenamiento o acceso técnico es necesario para la finalidad legítima de almacenar preferencias no solicitadas por el abonado o usuario.

Estadísticas

El almacenamiento o acceso técnico que es utilizado exclusivamente con fines estadísticos.El almacenamiento o acceso técnico que se utiliza exclusivamente con fines estadísticos anónimos. Sin un requerimiento, el cumplimiento voluntario por parte de tu proveedor de servicios de Internet, o los registros adicionales de un tercero, la información almacenada o recuperada sólo para este propósito no se puede utilizar para identificarte.

Marketing

El almacenamiento o acceso técnico es necesario para crear perfiles de usuario para enviar publicidad, o para rastrear al usuario en una web o en varias web con fines de marketing similares.