Fraud in bank payments: What’s happening in the U.S. and how to address it

Latinia

•14 de January de 2025•6 min read

The rapid advancement of technology has profoundly transformed how we interact with money, enabling online payments, instant transactions, and more accessible financial services. However, this digitalization has also paved the way for new forms of fraud, ranging from credit card data theft during online transactions to the creation of fraudulent websites designed to deceive users. These threats, along with traditional forms of fraud, pose an increasing challenge for financial institutions and consumers alike.

With alarming figures placing the U.S. as the country with the highest percentage of fraud-related losses compared to the rest of the world, it’s clear that current prevention strategies are falling short. This scenario raises critical questions: what factors explain the high incidence of fraud in the U.S.? What lessons can be learned from other regions, such as Europe, that have significantly curbed this issue?

In this article, we’ll examine the latest statistics on payment fraud, delve into the primary causes behind this problem, and highlight emerging technologies that could become key allies for banking institutions.

Bank Fraud Data in the U.S. and Globally

According to the It’s a Fraudster’s World report, global fraud losses amount to $211 billion, with one in five adults (21%) falling victim to some form of scam over the past three years.

One of the most common types of fraud involves payments, particularly card-related fraud. McKinsey estimates that global losses from payment card fraud will reach $400 billion over the next decade. Within this context, authorized push payment (APP) fraud is expected to grow at a compound annual growth rate (CAGR) of 11% through 2027, underscoring the challenges financial systems face worldwide.

The U.S. stands out negatively in this landscape:

In 2023, card fraud losses in the U.S. amounted to $14.32 billion, accounting for over 42% of global losses.

Despite U.S.-issued cards representing only one-quarter of the global card volume (according to the Nilson Report), the country’s losses were disproportionately high.

Losses in the S. averaged 11.01 cents per $100 in card volume—nearly double the global average of 6.58 cents.

Factors Behind the High Fraud Rate in the U.S.

The high percentage of fraud in the United States, compared to other regions, is driven by a combination of structural, technological, and regulatory factors.

Prevalence of Card-Not-Present (CNP) Transactions

The volume of CNP transactions has grown significantly. According to a 2021 PULSE study, these transactions increased by 23% and now account for one-third of all debit transactions in the U.S.

CNP transactions, primarily used in e-commerce, lack robust security measures like chip-based authentication, which protects in-person transactions. This vulnerability makes them an attractive target for fraudsters, who can exploit stolen card data to make online purchases without needing to physically verify the cardholder’s identity.

The Impact of E-commerce Growth on Fraud Vulnerability

E-commerce remains one of the primary drivers of CNP transactions, significantly increasing fraud vulnerability. According to Precedence Research, the global e-commerce market surpassed $16.29 trillion in 2023 and is projected to reach $75.12 trillion by 2034.

McKinsey highlights that CNP transactions continue to rise as consumers increasingly favor fast and convenient online shopping. However, this rapid expansion has not been accompanied by widespread adoption of advanced security measures, leaving significant gaps in the system’s defenses.

Lack of Measures Similar to Those Adopted in Other Regions

Compared to Europe, where the Payment Services Directive 2 (PSD2) and its Strong Customer Authentication (SCA) requirements have significantly reduced online payment fraud, the United States lacks an equivalent regulatory framework.

While initiatives and laws such as the GLBA, CCPA, and CFPB promote consumer protection and data security, the U.S. regulatory landscape remains more fragmented and less robust in combating fraud.

For example:

Open Banking: In Europe, PSD2 mandates that financial institutions provide secure API access to data. In the U.S., this practice largely depends on individual banks’ initiatives and is not supported by a regulatory mandate.

Authentication and Payment Protection: PSD2 requires multifactor authentication for all electronic transactions, whereas the U.S. has no equivalent regulation enforcing similar measures uniformly.

This fragmented approach leaves consumers and merchants with inconsistent protections against fraud. Additionally, while technological advancements in the U.S. payments ecosystem—such as real-time payment networks and the rise of fintech—have made transactions faster and more convenient, they have not been paired with uniform regulations to ensure security and trust across the system.

Current Anti-Fraud Measures in the U.S.

The United States has implemented various strategies to combat payment fraud, though these have proven limited given the scale of the issue.

One of the most significant steps has been the introduction of EMV chip technology (Europay, MasterCard, and Visa), which has effectively reduced in-person transaction fraud by making card cloning more difficult. However, this technology does not address the growing problem of CNP transactions, which represent a significant portion of current fraud cases.

In terms of regulation, the U.S. has laws and initiatives focused on consumer protection and data security, such as:

Gramm-Leach-Bliley Act (GLBA): Requires financial institutions to explain their data-sharing practices and protect customers’ financial information.

Consumer Financial Protection Bureau (CFPB): Ensures transparency and protects consumer rights in financial services.

However, these regulations are not as specific or uniform as measures adopted in other regions. While some state-level initiatives have introduced higher standards for privacy and data protection, they are not specifically designed to address payment fraud and are not applied nationwide.

Lessons from Europe: The Impact of PSD2 and SCA

Implemented in 2018, PSD2 aims to promote competition and innovation in the financial sector while enhancing consumer protection. One of its most notable elements is SCA, which requires transaction authentication using at least two out of three factors: something the user knows, possesses, or is.

These measures have proven effective in reducing fraud and strengthening trust in digital payments.

Successful Examples of Fraud Reduction in the EU

The measures introduced by PSD2 have proven highly effective. According to the European Banking Authority (EBA) report, fraud in credit transfers has dropped to just 0.0008% of the total transaction value, while card transactions show a fraud rate of 0.029% in value. Moreover, during the SCA migration period between 2020 and 2021, card payment fraud rates decreased by 40% to 60%.

A notable example is the reduction in fraud for remote card payments, directly attributed to the implementation of SCA by payment service providers and online merchants. By 2022, SCA was applied to70% of remote transfers and 36% of remote card transactions, significantly enhancing security in e-commerce.

Possibilities for Implementing Similar Measures in the U.S.

Although the United States does not have an equivalent framework to PSD2, adopting similar measures could significantly reduce fraud. Implementing a national multifactor authentication standard inspired by SCA would enhance the security of electronic transactions and reduce the system’s vulnerability to sophisticated fraud schemes.

Additionally, the European approach to cooperation among financial institutions could serve as a valuable lesson. Creating fraud data-sharing platforms, as recommended by the EBA, would allow U.S. institutions to share information on fraud patterns and suspicious actors. This would enable a more coordinated and effective response to emerging threats.

Emerging Technologies to Combat Bank Fraud

While technology increases fraud risks, it also provides essential solutions to tackle them effectively. Recent advancements enable financial institutions to better protect their customers and strengthen transaction security by continually adapting to emerging threats.

Here are three key technologies transforming the sector:

3D Secure 2.0 (3DS2)

3D Secure 2.0 (3DS2) is a pivotal tool in this effort. This advanced system allows for real-time risk assessment, ensuring low-risk transactions proceed seamlessly while requiring additional authentication for suspicious ones. In Europe, its integration as part of SCA has proven highly effective in reducing fraud in remote card payments, a model that could be successfully replicated in other markets.

Tokenization

Tokenization adds another critical layer of security by replacing sensitive card data with unique identifiers, or “tokens.” This ensures that even if data is intercepted, it cannot be fraudulently reused. This approach is especially valuable in e-commerce, where the prevalence of card-not-present transactions increases the risk of fraud.

Advanced Data Analytics and Cybersecurity

Transactional data analysis and advanced cybersecurity solutions have transformed fraud prevention strategies. Real-time behavioral pattern analysis enables the detection and communication of suspicious activities before they cause harm.

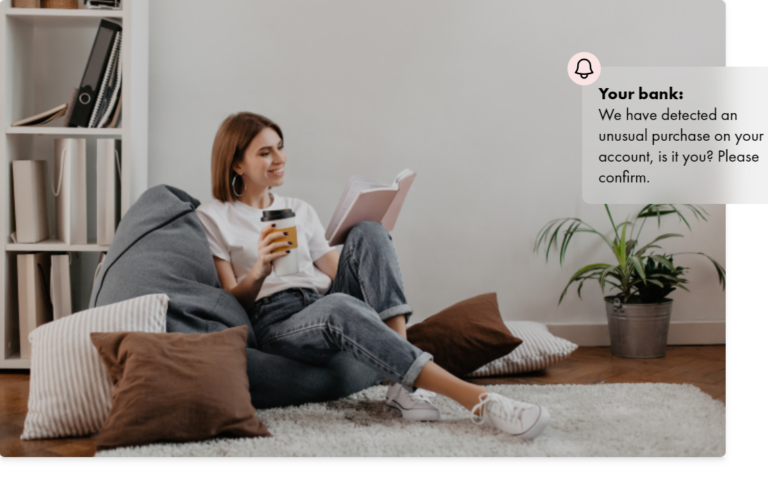

One of the most effective ways to enhance your bank’s security is by integrating advanced solutions like those offered by Latinia. Our technology, leveraging both historical and real-time data analysis, allows for immediate notification of any suspicious activity, such as unusual or high-value transactions. This instant communication enables customers to quickly confirm or deny operations, significantly reducing the risk of fraud.

Additionally, our Critical Event Gateway ensures that critical messages are delivered reliably and without delay. Whether it’s fraud alerts, OTP authorizations, or other important notifications, this system guarantees rapid customer responses, enhancing trust and effectively safeguarding the financial ecosystem.

The rapid advancement of technology has profoundly transformed how we interact with money, enabling online payments, instant transactions, and more accessible financial services. However, this…

The rapid advancement of technology has profoundly transformed how we interact with money, enabling online payments, instant transactions, and more accessible financial services. However, this…

The rapid advancement of technology has profoundly transformed how we interact with money, enabling online payments, instant transactions, and more accessible financial services. However, this…

The rapid advancement of technology has profoundly transformed how we interact with money, enabling online payments, instant transactions, and more accessible financial services. However, this…

The rapid advancement of technology has profoundly transformed how we interact with money, enabling online payments, instant transactions, and more accessible financial services. However, this…

The rapid advancement of technology has profoundly transformed how we interact with money, enabling online payments, instant transactions, and more accessible financial services. However, this…

The rapid advancement of technology has profoundly transformed how we interact with money, enabling online payments, instant transactions, and more accessible financial services. However, this…

The rapid advancement of technology has profoundly transformed how we interact with money, enabling online payments, instant transactions, and more accessible financial services. However, this…

The rapid advancement of technology has profoundly transformed how we interact with money, enabling online payments, instant transactions, and more accessible financial services. However, this…

The rapid advancement of technology has profoundly transformed how we interact with money, enabling online payments, instant transactions, and more accessible financial services. However, this…

The rapid advancement of technology has profoundly transformed how we interact with money, enabling online payments, instant transactions, and more accessible financial services. However, this…

The rapid advancement of technology has profoundly transformed how we interact with money, enabling online payments, instant transactions, and more accessible financial services. However, this…

Para ofrecer las mejores experiencias, utilizamos tecnologías como las cookies para almacenar y/o acceder a la información del dispositivo. El consentimiento de estas tecnologías nos permitirá procesar datos como el comportamiento de navegación o las identificaciones únicas en este sitio. No consentir o retirar el consentimiento, puede afectar negativamente a ciertas características y funciones.

Funcional

Always active

El almacenamiento o acceso técnico es estrictamente necesario para el propósito legítimo de permitir el uso de un servicio específico explícitamente solicitado por el abonado o usuario, o con el único propósito de llevar a cabo la transmisión de una comunicación a través de una red de comunicaciones electrónicas.

Preferencias

El almacenamiento o acceso técnico es necesario para la finalidad legítima de almacenar preferencias no solicitadas por el abonado o usuario.

Estadísticas

El almacenamiento o acceso técnico que es utilizado exclusivamente con fines estadísticos.El almacenamiento o acceso técnico que se utiliza exclusivamente con fines estadísticos anónimos. Sin un requerimiento, el cumplimiento voluntario por parte de tu proveedor de servicios de Internet, o los registros adicionales de un tercero, la información almacenada o recuperada sólo para este propósito no se puede utilizar para identificarte.

Marketing

El almacenamiento o acceso técnico es necesario para crear perfiles de usuario para enviar publicidad, o para rastrear al usuario en una web o en varias web con fines de marketing similares.