Regulatory Compliance and Fraud Prevention: The Role of AML in Banking

Latinia

•1 de May de 2025•6 min read

Regulatory compliance has become a strategic pillar for financial institutions, especially amid increasing regulatory demands and growing international pressure to prevent money laundering. In this context, AML (Anti-Money Laundering) policies are no longer just a legal obligation—they are now essential tools for protecting a bank’s reputation, ensuring operational stability, and strengthening customer trust.

This article provides a practical and updated overview of the role of AML in banking, covering how it works, key regulations, compliance strategies, and technological solutions that can make a real difference.

What Is AML and Why Is It Essential in Banking?

AML (Anti-Money Laundering) refers to a set of policies, processes, and technologies designed to prevent illicit funds from entering the financial system. Its implementation is mandatory for banks and other regulated institutions, which must detect, report, and prevent transactions potentially linked to criminal activities such as drug trafficking, corruption, or terrorism financing.

AML plays a critical role in the banking sector because of the central position financial institutions occupy in the global flow of capital. Banks process millions of transactions daily, and any weakness in their control systems can enable the legitimization of illicit funds, leading to serious economic and reputational consequences. According to estimates by the UNODC, between 2% and 5% of global GDP is laundered every year, representing between $800 billion and $2 trillion.

Institutions that fail to comply with AML regulations face steep penalties, a loss of customer trust, and significant legal risks. In 2023 alone, banks were fined $6.6 billion for violations related to AML, KYC, and other regulatory obligations (Fenergo, 2024).

Beyond legal requirements, AML has become a strategic priority. An effective program not only ensures regulatory compliance but also helps safeguard the integrity of the financial system, deters organized crime, and reinforces the bank’s credibility with customers, investors, and regulators.

How Does AML Work in the Financial Sector?

Anti-money laundering efforts in banking rely on a series of controls designed to prevent illicit funds from entering and moving through the financial system. These controls not only help detect potential criminal activity but also ensure compliance with national and international regulations, while protecting the integrity of the banking ecosystem.

AML processes are generally structured around the three key stages of money laundering:

Placement: Illicit funds are introduced into the financial system. This can occur through cash deposits, falsified invoice payments, or by breaking up large sums into smaller amounts spread across various accounts—a tactic known as smurfing—to avoid detection.

Layering: Multiple transactions are carried out to obscure the origin of the funds. Common techniques include transfers between accounts in different jurisdictions, the use of shell companies, or the buying and selling of assets to hide the money trail.

Integration: Once “cleaned,” the funds are reintroduced into the economy with the appearance of legitimacy. At this stage, the money may be used to purchase real estate, invest in financial instruments, or fund business activities.

To prevent this cycle from completing, financial institutions implement a range of measures—such as identity verification (Know Your Customer or KYC)—which we’ll explore later in this article.

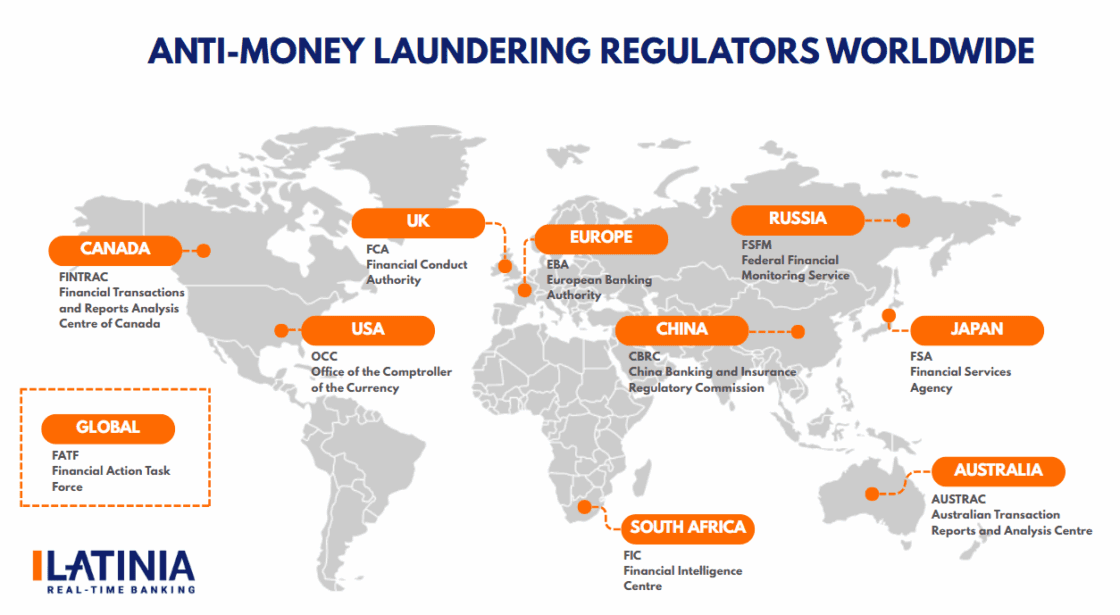

Anti-money laundering regulations and regulators

Compliance with AML regulations in the banking sector takes place within a global landscape that is constantly evolving. While rules differ across regions, they all share the same core objective: to stop the flow of illicit funds, protect the integrity of the financial system, and prevent crimes such as corruption, fraud, and terrorist financing.

Europe

The European regulatory framework is built around Anti-Money Laundering Directives (AMLD). Currently, the Sixth Anti-Money Laundering Directive (6AMLD) significantly strengthens control mechanisms by expanding the list of predicate offenses, toughening penalties, and enabling the criminal prosecution of legal entities, including corporations. Efforts are also underway to establish a European AML supervisory authority, driven by countries such as Germany, Spain, Italy, and the Netherlands, with a strong focus on regulating digital assets.

North America (U.S. and Canada)

In the United States, AML regulations are primarily shaped by the Bank Secrecy Act (BSA), enacted in 1970, and reinforced by the Anti-Money Laundering Act of 2020 (AMLA). This act represents the most significant update since the Patriot Act, introducing measures to eliminate shell companies and expanding regulatory oversight to sectors like art and cryptocurrencies. Oversight and enforcement fall to the Financial Crimes Enforcement Network (FinCEN), which received over 4.6 million Suspicious Activity Reports (SARs) in 2023.

In Canada, AML enforcement is led by the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC). The agency monitors compliance across key sectors such as banking, insurance, casinos, real estate, and cryptocurrency platforms, all of which are subject to strict regulatory scrutiny.

Latin America

Latin America has strengthened its regulatory frameworks to align with international standards promoted by organizations such as the Financial Action Task Force (FATF) and the United Nations Office on Drugs and Crime (UNODC). Countries like Mexico, Colombia, Brazil, Chile, and Peru have enacted specific legislation that requires financial institutions to implement formal anti-money laundering policies.

Strategies for Ensuring AML Compliance in Banking

Complying with AML regulations requires more than basic controls—it demands a proactive and structured approach that enables financial institutions to identify risks, act quickly, and adapt to evolving regulatory frameworks.

Below are the key strategies that help strengthen compliance in the banking sector.

Ongoing Risk Assessments

Risk assessment should not be a one-time task. Banks must conduct continuous reviews that cover customer behavior, the nature of the products and services offered, and relationships with third parties such as ultimate beneficial owners.

Robust Customer Identification and Verification (KYC)

A strong identity verification process is the first step in preventing financial crimes. Banks must collect and validate data such as name, address, date of birth, and beneficial ownership, using both traditional methods and advanced digital solutions. This process is mandatory before establishing any business relationship.

Continuous Transaction Monitoring

Ongoing transaction monitoring helps detect unusual activity or suspicious behavior patterns. This includes monitoring transactions that exceed certain thresholds and analyzing repeated low-value transfers that may signal smurfing techniques.

Use of Alternative Data and New Technologies

Leveraging alternative data—such as a user’s digital footprint, IP analysis, or email verification—adds an extra layer of protection when validating clients and detecting risk. This data complements traditional sources and improves the quality of due diligence.

Risk-Based AML Policies

Banks should develop AML policies that not only meet regulatory requirements but are also customer-centric, tailored to each specific risk profile. This involves adjusting controls based on factors such as economic activity, source of funds, or country of residence.

Advanced Monitoring and Analytics Solutions

The implementation of cutting-edge technology—like real-time transactional data monitoring platforms, rule engines powered by machine learning, and automated identity verification tools—helps optimize AML processes, reduce errors, and accelerate responses to risk.

Ongoing Staff Training

Continuous staff education is essential to keep AML programs effective. All employees must understand their role in risk detection and stay informed about emerging threats and regulatory updates.

Effective Collaboration with Regulatory Authorities

Maintaining open communication channels with regulatory bodies and cooperating in the detection and investigation of suspicious activities strengthens a bank’s compliance posture and reinforces its commitment to financial integrity.

Advanced Solutions to Strengthen AML Programs

The use of advanced technologies has become essential for banks to meet AML requirements in a faster, more efficient, and secure way. As transaction volumes increase and financial crimes grow more sophisticated, automating processes, analyzing data in real time, and ensuring traceable communications make a critical difference.

Some of the most impactful solutions for enhancing AML programs include:

Real-time monitoring systems: These tools detect suspicious patterns instantly, helping avoid delays in responding to potentially illicit activity.

Decision engines powered by customer intelligence: By analyzing each user’s transactional behavior, these engines can identify risks and trigger automatic actions like account blocks or requests for further verification.

Automated critical communications: Notifying customers in real time about anomalies in their accounts is key to preventing fraud and minimizing impact.

In this context, Latinia brings a unique advantage to meeting security and compliance requirements. A specialist in real-time decision software for the banking industry, Latinia provides financial institutions with a powerful solution that combines transactional analysis with real-time communication.

It’s not just about sending alerts—Latinia offers a decision engine capable of:

Instantly analyzing transactional events to detect unusual activity.

Supporting fraud prevention by immediately sending security alerts, such as notifications of suspicious logins or attempted identity theft.

Ensuring regulatory compliance by maintaining complete traceability of critical messages sent to clients, which can be vital in audits or dispute resolution.

Integrating seamlessly with existing systems to accelerate the adoption of more effective AML practices.

With Latinia, banks not only strengthen their ability to meet regulatory demands—they also proactively protect their customers, build greater trust, and enhance the overall integrity of the financial system.

Regulatory compliance has become a strategic pillar for financial institutions, especially amid increasing regulatory demands and growing international pressure to prevent money laundering. In this…

Regulatory compliance has become a strategic pillar for financial institutions, especially amid increasing regulatory demands and growing international pressure to prevent money laundering. In this…

Regulatory compliance has become a strategic pillar for financial institutions, especially amid increasing regulatory demands and growing international pressure to prevent money laundering. In this…

Regulatory compliance has become a strategic pillar for financial institutions, especially amid increasing regulatory demands and growing international pressure to prevent money laundering. In this…

Regulatory compliance has become a strategic pillar for financial institutions, especially amid increasing regulatory demands and growing international pressure to prevent money laundering. In this…

Regulatory compliance has become a strategic pillar for financial institutions, especially amid increasing regulatory demands and growing international pressure to prevent money laundering. In this…

Regulatory compliance has become a strategic pillar for financial institutions, especially amid increasing regulatory demands and growing international pressure to prevent money laundering. In this…

Regulatory compliance has become a strategic pillar for financial institutions, especially amid increasing regulatory demands and growing international pressure to prevent money laundering. In this…

Regulatory compliance has become a strategic pillar for financial institutions, especially amid increasing regulatory demands and growing international pressure to prevent money laundering. In this…

Regulatory compliance has become a strategic pillar for financial institutions, especially amid increasing regulatory demands and growing international pressure to prevent money laundering. In this…

Regulatory compliance has become a strategic pillar for financial institutions, especially amid increasing regulatory demands and growing international pressure to prevent money laundering. In this…

Regulatory compliance has become a strategic pillar for financial institutions, especially amid increasing regulatory demands and growing international pressure to prevent money laundering. In this…

Para ofrecer las mejores experiencias, utilizamos tecnologías como las cookies para almacenar y/o acceder a la información del dispositivo. El consentimiento de estas tecnologías nos permitirá procesar datos como el comportamiento de navegación o las identificaciones únicas en este sitio. No consentir o retirar el consentimiento, puede afectar negativamente a ciertas características y funciones.

Funcional

Always active

El almacenamiento o acceso técnico es estrictamente necesario para el propósito legítimo de permitir el uso de un servicio específico explícitamente solicitado por el abonado o usuario, o con el único propósito de llevar a cabo la transmisión de una comunicación a través de una red de comunicaciones electrónicas.

Preferencias

El almacenamiento o acceso técnico es necesario para la finalidad legítima de almacenar preferencias no solicitadas por el abonado o usuario.

Estadísticas

El almacenamiento o acceso técnico que es utilizado exclusivamente con fines estadísticos.El almacenamiento o acceso técnico que se utiliza exclusivamente con fines estadísticos anónimos. Sin un requerimiento, el cumplimiento voluntario por parte de tu proveedor de servicios de Internet, o los registros adicionales de un tercero, la información almacenada o recuperada sólo para este propósito no se puede utilizar para identificarte.

Marketing

El almacenamiento o acceso técnico es necesario para crear perfiles de usuario para enviar publicidad, o para rastrear al usuario en una web o en varias web con fines de marketing similares.