Hyper-personalization as operational safeguard for banking

Latinia

•21 de August de 2025•6 min read

Can hyper-personalization help banks meet regulatory requirements and strengthen their operational resilience?

By 2025, hyper-personalization has become one of the most solid strategic bets in the financial sector. But beyond delivering a tailored experience, can this technology also help banks comply with demanding regulations—such as PSD3, MiCA, or DORA—while strengthening their operational resilience?

The answer starts to take shape in the way the most innovative players manage their data, automate decision-making, and communicate with precision at critical moments. In an increasingly regulated and digital environment, predictive analytics, artificial intelligence, and resilient messaging platforms are playing an increasingly decisive role.

Context: Between Customer Expectations and Regulatory Pressure

More than ever, customers expect their banks to deliver the same agility and personalization they receive from other digital sectors. They look for interactions that recognize their history, needs, and context—while providing immediate value. This goes beyond offering tailored recommendations or products; it also means delivering timely, adapted communications when regulatory changes occur, risks are detected, or specific actions require their attention.

Today’s banking industry operates under constant tension: it must adapt to increasingly strict regulatory frameworks while keeping up with rising expectations for personalization and agility, driven by major digital platforms.

In Europe, the PSD3 directive introduces tougher standards to fight digital fraud, requires strong customer authentication (SCA), and promotes greater payment transparency. MiCA regulates crypto-assets with consumer protection and disclosure requirements.

In the United States, OCC, the Fed, and FINRA are moving forward with technology supervision, focusing on cybersecurity and automation.

Meanwhile, Latin America faces the challenge of harmonizing increasingly sophisticated regulatory frameworks while meeting growing technological demands and expanding digital offerings.

Within this context, hyper-personalization—traditionally linked to marketing—takes on a new role: anticipating risks, adapting critical alerts, and ensuring regulatory compliance in an automated and contextualized way.

Where Does Banking Personalization Stand Today?

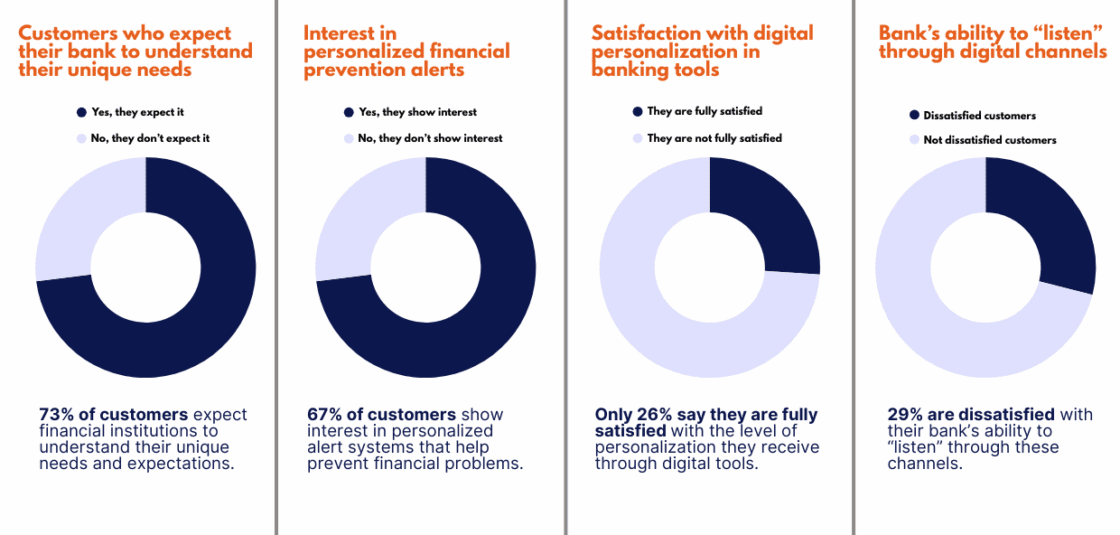

Although personalization has been on the agenda of financial institutions for years, its true level of maturity still shows clear gaps.

According to the Digital Banking Experience Report 2022 and Funds Society, customers expect their bank to understand their needs and value personalized alerts, but only a minority feel fully satisfied with the personalization they receive. These findings highlight that many banks still rely on marketing automation systems that ignore the customer’s real transactional context, resulting in generic and less relevant communications.

In institutions with more advanced personalization strategies, these capabilities are no longer limited to marketing—they are also applied in critical areas such as fraud prevention, alert traceability, and adapting messages to specific regulatory requirements.

From Personalization to Protection: A Paradigm Shift

Applying advanced analytics and big data technologies makes it possible to adapt every banking interaction to the customer’s unique circumstances and context. This has direct implications for regulatory compliance:

Fraud detection and real-time monitoring (PSD3): Identifying unusual behavior patterns and triggering immediate alerts before damage occurs serves both an operational and regulatory function.

Transparency and financial education (MiCA & US platforms): Personalized notifications help inform customers about the risks tied to complex products such as crypto-assets or loans, aligning with the goal of keeping consumers informed.

Evidence for regulators (DORA, GDPR): Every message delivered must be auditable, traceable, and prioritized. Here, notification and automation platforms play a key role in maintaining operational traceability.

Hyper-personalization not only enhances customer relationships but also strengthens two critical pillars of the financial sector: regulatory compliance and operational resilience.

These two are deeply connected: a more resilient institution can demonstrate stronger control over its operations to regulators, while also ensuring customers a safe, contextualized experience:

Better automated and adaptable decisions in times of crisis, enabled by real-time granular segmentation.

Anticipation of needs and shifts in financial behavior through contextual and predictive experiences.

Reduced exposure to defaults or fraud with dynamic offers aligned to each risk profile.

Lower reliance on manual operations, powered by intelligent automation (chatbots, recommendation engines).

Stronger decision-making in volatile environments thanks to integrated and well-governed data.

In this way, hyper-personalization goes beyond marketing and becomes a structural mechanism to:

Comply with demanding regulatory frameworks (PSD3, MiCA, DORA…).

Ensure operational continuity, even under high-pressure or crisis scenarios.

Protect both the customer and the institution from financial, reputational, or regulatory risks.

By combining behavioral analytics, real-time triggers, and automated decision layers—such as Latinia’s NBA engine—regulated communications can be turned into useful actions that deliver compliance value and safeguard reputation.

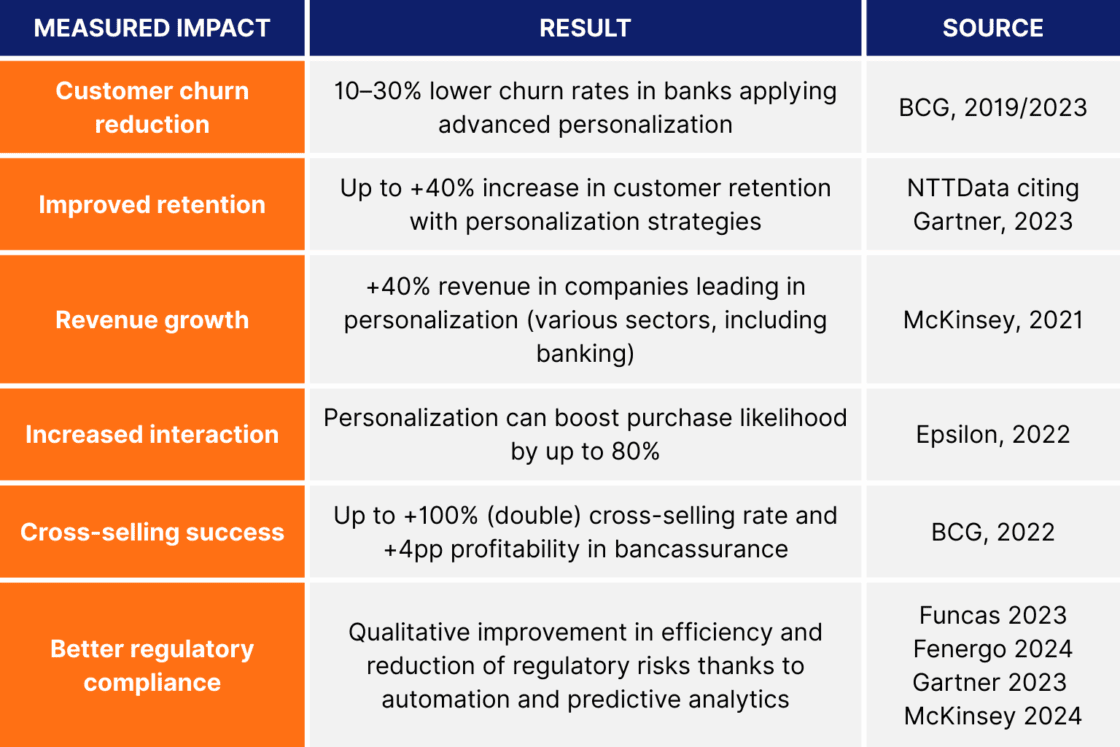

Business Impact and Resilience: Measured Results

The relevance of hyper-personalization is also reflected in quantitative metrics.

Below are data showing how hyper-personalization impacts business performance—improving retention, revenue, interaction, cross-selling, and regulatory compliance.

Real Cases: How Banks Are Acting Today

Bank of America (USA): Integrated its virtual assistant Erica into a hyper-personalization strategy that successfully handles over 8 million weekly interactions, boosting customer satisfaction while meeting regulatory standards for consumer protection.

BBVA (Europe & LatAm): Recognized as an international leader in advanced analytics, BBVA has enhanced the personalization of transactional alerts and the detection of suspicious activities, combining fraud control with regulatory compliance.

Banco Azteca (Mexico): Rolled out a hyper-personalization strategy that merges online and offline data to adjust customer experiences in real time. As a result, it achieved a 178% increase in financial product sales, a 30% reduction in cost per action, and a 69% growth in new personal credit accounts.

Commonwealth Bank of Australia (Australia): Uses its Customer Engagement Engine, a platform that processes hundreds of billions of data points in real time to generate hyper-personalized interactions. It delivers contextual recommendations and offers at the right moment, increasing engagement and earning international recognition such as the Celent Model Bank Award.

Royal Bank of Canada (Canada): Integrated the NOMI suite into its app, featuring Insights (habit analysis), Find & Save (automatic savings), and Budgets (smart budgeting). In just a few months, users viewed more than 100 million insights, app usage grew 20%, and savings doubled compared to traditional products.

*Insights = personalized in-app notifications generated from customer transactional data analysis.

United Overseas Bank (Singapore): Developed 171 personalized insights specifically tailored to each customer. This drove remarkable engagement results: a 400% increase in customer interaction, a higher Net Promoter Score, a 50% click-through rate (CTR) on insights, and nearly two-thirds of new customers joined through referrals from existing ones.

Hyundai Card (South Korea): Implemented more than 100 hyper-personalized insights. This resulted in a 19% monthly CTR on calls-to-action based on those insights and outstanding customer ratings: 4.8 out of 5.

Emirates NBD (United Arab Emirates): Transformed its More app into a lifestyle ecosystem with hyper-personalized offers powered by advanced analytics, achieving more than 30,000 downloads and strengthening brand loyalty.

The Resilient Layer: The Role of Critical Notifications

Resilience doesn’t start or end in a data center or with channel and provider balancing. True banking resilience is activated when a critical alert reaches the right customer, through the right channel, at the right moment.

Latinia’s product, specialized in transactional and regulatory banking alerts, has proven its resilience by strengthening critical communications in highly regulated environments. We work with financial institutions to deliver context-aware banking alerts—via push notifications, SMS, WhatsApp, and email—integrated with real-time decision engines and adaptive protocols that ensure both continuity and regulatory compliance.

Key capabilities that enable this level of service include:

High availability and operational continuity, ensuring notification delivery even during incidents or peak pressure moments.

Full traceability, providing clear evidence for auditors or regulators.

Intelligent prioritization, distinguishing critical alerts—such as fraud, account blocks, or authentication—from informational or commercial communications.

Strong regulatory flexibility, adapting content, channels, and authorizations to both local and international requirements.

Conclusion: Hyper-personalization Is Not Optional, It’s Structural

Can hyper-personalization contribute to regulatory compliance and operational resilience?

Yes—it already is. With the support of specialized platforms like Latinia, which combine speed, context, and consistency in alert management, banks can automate regulatory compliance, protect customers, and even prevent reputational or systemic crises.

In 2025, hyper-personalization is not a luxury feature—it’s a structural element of the banking operating model. It represents the natural evolution of an industry that can no longer separate customer experience from compliance, nor communication from resilience.

Banks that view hyper-personalization as part of their operational infrastructure—and not just as a marketing tool—will be the ones to achieve greater resilience, relevance, and competitiveness in today’s financial landscape.

Want to strengthen continuity, traceability, and effectiveness of your bank’s notifications through hyper-personalization? Learn more about our resilient functionalities or reach out to a Latinia expert for more details.

Can hyper-personalization help banks meet regulatory requirements and strengthen their operational resilience?

By 2025, hyper-personalization has become one of the most solid strategic bets in the…

Can hyper-personalization help banks meet regulatory requirements and strengthen their operational resilience?

By 2025, hyper-personalization has become one of the most solid strategic bets in the…

Can hyper-personalization help banks meet regulatory requirements and strengthen their operational resilience?

By 2025, hyper-personalization has become one of the most solid strategic bets in the…

Can hyper-personalization help banks meet regulatory requirements and strengthen their operational resilience?

By 2025, hyper-personalization has become one of the most solid strategic bets in the…

Can hyper-personalization help banks meet regulatory requirements and strengthen their operational resilience?

By 2025, hyper-personalization has become one of the most solid strategic bets in the…

Can hyper-personalization help banks meet regulatory requirements and strengthen their operational resilience?

By 2025, hyper-personalization has become one of the most solid strategic bets in the…

Can hyper-personalization help banks meet regulatory requirements and strengthen their operational resilience?

By 2025, hyper-personalization has become one of the most solid strategic bets in the…

Can hyper-personalization help banks meet regulatory requirements and strengthen their operational resilience?

By 2025, hyper-personalization has become one of the most solid strategic bets in the…

Can hyper-personalization help banks meet regulatory requirements and strengthen their operational resilience?

By 2025, hyper-personalization has become one of the most solid strategic bets in the…

Can hyper-personalization help banks meet regulatory requirements and strengthen their operational resilience?

By 2025, hyper-personalization has become one of the most solid strategic bets in the…

Can hyper-personalization help banks meet regulatory requirements and strengthen their operational resilience?

By 2025, hyper-personalization has become one of the most solid strategic bets in the…

Can hyper-personalization help banks meet regulatory requirements and strengthen their operational resilience?

By 2025, hyper-personalization has become one of the most solid strategic bets in the…

Para ofrecer las mejores experiencias, utilizamos tecnologías como las cookies para almacenar y/o acceder a la información del dispositivo. El consentimiento de estas tecnologías nos permitirá procesar datos como el comportamiento de navegación o las identificaciones únicas en este sitio. No consentir o retirar el consentimiento, puede afectar negativamente a ciertas características y funciones.

Funcional

Always active

El almacenamiento o acceso técnico es estrictamente necesario para el propósito legítimo de permitir el uso de un servicio específico explícitamente solicitado por el abonado o usuario, o con el único propósito de llevar a cabo la transmisión de una comunicación a través de una red de comunicaciones electrónicas.

Preferencias

El almacenamiento o acceso técnico es necesario para la finalidad legítima de almacenar preferencias no solicitadas por el abonado o usuario.

Estadísticas

El almacenamiento o acceso técnico que es utilizado exclusivamente con fines estadísticos.El almacenamiento o acceso técnico que se utiliza exclusivamente con fines estadísticos anónimos. Sin un requerimiento, el cumplimiento voluntario por parte de tu proveedor de servicios de Internet, o los registros adicionales de un tercero, la información almacenada o recuperada sólo para este propósito no se puede utilizar para identificarte.

Marketing

El almacenamiento o acceso técnico es necesario para crear perfiles de usuario para enviar publicidad, o para rastrear al usuario en una web o en varias web con fines de marketing similares.