3 Steps to Successful Bank Card Promotion Based on a Next Best Action Strategy

Latinia

•4 de April de 2023•6 min read

Financial institutions have a significant impact on the financial lives of their cardholders, but this is a mutual relationship. Cardholders also possess the power to shape business practices and affect the types of products offered. It is crucial to consider both perspectives to leverage real-time revenue moments and untapped opportunities.

How the Next Best Action Approach Can Help Your Bank Succeed

Most financial institutions have more data than they know what to do with. Advancements in customer experience platforms and automation tools have made it easier to utilize and apply data as part of marketing strategies for financial services. However, most banks invest in intent data – that is, the data that allows you to see behaviors that may indicate intent to buy. While this data is crucial to marketing and selling today, it doesn’t tell the whole story.

By utilizing a Next Best Action (NBA) approach for the promotion of card products, financial organizations can take advantage of real-time revenue moments and untapped opportunities, including attracting new cardholders, activating those who have gone dormant, and finding incentives that increase business from active customers.

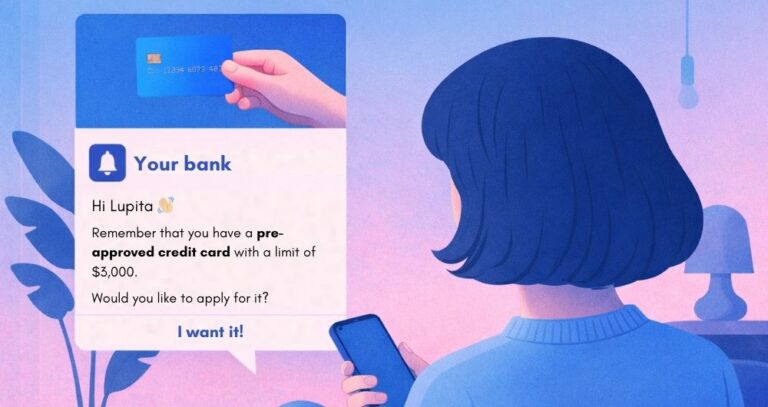

NBA systems can make use of valuable information obtained from user transactions. Latinia’s NBA decision engine enables banks to promote products to customers in real-time, engaging with them immediately when a relevant transaction is detected, if the customer meets the pre-established demographic and contractual criteria.

The difficulty lies in identifying which current cardholders to focus on and determining the behavior modifications required to create added value. Banks and credit unions can achieve this through three steps. The first step belongs to customers who have recently opened credit card accounts with the institution.

1. Engage early and often with new cardholders

The credit card market is highly competitive. Consumers have numerous options and receive multiple offers. Given the abundance of alternatives, it is crucial to establish loyalty with your cardholders by building strong relationships and trust. Attempting to take shortcuts is unfeasible and will not prove beneficial in the long term.

Establishing a robust cardholder relationship during the first 45 days after opening a new credit card account is crucial. An “early-month” onboard program can reinforce the credit card’s value proposition and encourage usage, leading to the development of spending habits that position the card as top of wallet.

2. Prioritize current cardholders with the potential for increased spending

Financial institutions may be tempted to target their most active and valuable cardholders with offers. However, it can be challenging to generate additional spending from this group, particularly if the institution’s credit card already has the largest share of wallet.

Alternatively, the focus should be on retaining this segment by providing constant recognition and top customer service.

3. Adjust offers to incentivize desired behavior

After defining the target audience, the next question is, “How can we tap into the cardholder potential?” Merchant category and promotional offers can be highly effective if the strategy is aligned with the desired shift in cardholder behavior.

Financial institutions have a significant impact on the financial lives of their cardholders, but this is a mutual relationship. Cardholders also possess the power to shape business practices and…

Financial institutions have a significant impact on the financial lives of their cardholders, but this is a mutual relationship. Cardholders also possess the power to shape business practices and…

Financial institutions have a significant impact on the financial lives of their cardholders, but this is a mutual relationship. Cardholders also possess the power to shape business practices and…

Financial institutions have a significant impact on the financial lives of their cardholders, but this is a mutual relationship. Cardholders also possess the power to shape business practices and…

Financial institutions have a significant impact on the financial lives of their cardholders, but this is a mutual relationship. Cardholders also possess the power to shape business practices and…

Financial institutions have a significant impact on the financial lives of their cardholders, but this is a mutual relationship. Cardholders also possess the power to shape business practices and…

Financial institutions have a significant impact on the financial lives of their cardholders, but this is a mutual relationship. Cardholders also possess the power to shape business practices and…

Financial institutions have a significant impact on the financial lives of their cardholders, but this is a mutual relationship. Cardholders also possess the power to shape business practices and…

Financial institutions have a significant impact on the financial lives of their cardholders, but this is a mutual relationship. Cardholders also possess the power to shape business practices and…

Financial institutions have a significant impact on the financial lives of their cardholders, but this is a mutual relationship. Cardholders also possess the power to shape business practices and…

Financial institutions have a significant impact on the financial lives of their cardholders, but this is a mutual relationship. Cardholders also possess the power to shape business practices and…

Financial institutions have a significant impact on the financial lives of their cardholders, but this is a mutual relationship. Cardholders also possess the power to shape business practices and…

Para ofrecer las mejores experiencias, utilizamos tecnologías como las cookies para almacenar y/o acceder a la información del dispositivo. El consentimiento de estas tecnologías nos permitirá procesar datos como el comportamiento de navegación o las identificaciones únicas en este sitio. No consentir o retirar el consentimiento, puede afectar negativamente a ciertas características y funciones.

Funcional

Always active

El almacenamiento o acceso técnico es estrictamente necesario para el propósito legítimo de permitir el uso de un servicio específico explícitamente solicitado por el abonado o usuario, o con el único propósito de llevar a cabo la transmisión de una comunicación a través de una red de comunicaciones electrónicas.

Preferencias

El almacenamiento o acceso técnico es necesario para la finalidad legítima de almacenar preferencias no solicitadas por el abonado o usuario.

Estadísticas

El almacenamiento o acceso técnico que es utilizado exclusivamente con fines estadísticos.El almacenamiento o acceso técnico que se utiliza exclusivamente con fines estadísticos anónimos. Sin un requerimiento, el cumplimiento voluntario por parte de tu proveedor de servicios de Internet, o los registros adicionales de un tercero, la información almacenada o recuperada sólo para este propósito no se puede utilizar para identificarte.

Marketing

El almacenamiento o acceso técnico es necesario para crear perfiles de usuario para enviar publicidad, o para rastrear al usuario en una web o en varias web con fines de marketing similares.