In recent years, we have witnessed a significant increase in cyberattacks. According to Cybersecurity Ventures, cybercrime is booming: by the end of 2023, it could have an impact of close to $8 trillion globally and the forecast for 2025 is $10.5 trillion. Social engineering techniques, in particular, have become more prevalent and sophisticated, with cybercriminals using them to gain unauthorized access to our data. This highlights the fact that consumers are still the primary targets of such attacks.

Although it may seem counterintuitive, people are the weakest link in the chain when it comes to ensuring a bank’s cybersecurity, rather than technology alone. In our recent cybersecurity perception poll, 75% of respondents expressed confidence in their ability to keep themselves and their data secure online. The report COVID-19 Clicks: How Phishing Capitalized on a Global Crisis also reveals that this false sense of confidence is indeed worldwide.

Three Actions to Prevent Security Breaches in Banking

Banks should prioritize proactive cybersecurity measures in order to protect their customers’ assets and enhance the overall customer experience. Taking a comprehensive approach to cybersecurity is important not only to meet regulatory compliance, but also to safeguard against potential threats.

1. Education and Awareness

Implementing customer awareness initiatives is a crucial best practice for effective banking cybersecurity. Not only is it a simple approach, but it is also highly effective in preventing security breaches. By providing customers with proper education and tools, they can better protect themselves and ultimately, the bank as well.

It’s essential to educate customers on the following:

- Recognizing fraud and identifying suspicious activity

- Understanding the basic types of breaches

- Knowing what actions to take if they fall victim to a cyber attack

Investing in customer education can help block common cybercriminal tactics, such as phishing and malware, and significantly improve overall cybersecurity.

2. Security Technology Implementation

One way to do this is by setting up OTP (One-Time Password) and 2FA (Two-Factor Authentication) protocols for online payments. These security measures add an extra layer of protection, ensuring that only authorized individuals can access the account and conduct transactions.

Biometric authentication is another highly secure option, which utilizes unique physical attributes such as fingerprints, facial recognition, or iris scans to confirm a user’s identity.

3. Engagement and Empowerment

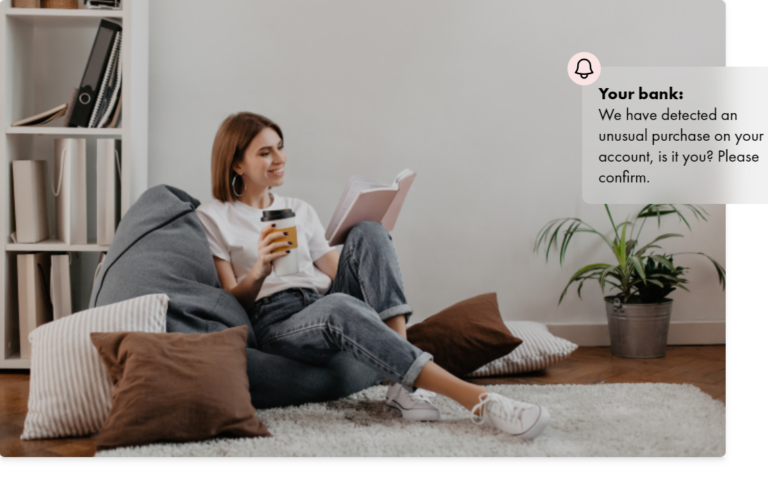

Encouraging customer engagement and empowerment is essential in preventing fraud and providing them with communication tools is a key component of this approach. By offering real-time notifications and giving customers the power to decide when and how they receive them, banks can empower their clients to act quickly in the event of a potential security threat. This not only enhances customer experience but also increases the likelihood of fraud prevention.

By engaging customers in the prevention of fraud, banks can encourage a sense of shared responsibility, where customers are actively involved in protecting their own assets. This approach can be highly effective in preventing fraud, as it raises awareness and promotes vigilance. It also demonstrates to customers that the bank is committed to their safety and security.