Customer Segmentation in Banking: Impact Strategies 2026

Latinia

•2 de November de 2023•6 min read

In banking, customer segmentation is more than just a tool; it’s the central strategy for effectively connecting with our users and their needs. Each customer, with their unique demands and financial habits, presents us with the challenge of understanding them and, even more so, tailoring our offerings in a way that is genuinely relevant to them.

In this article, we will:

Explore effective customer segmentation in the banking sector.

Analyze the differences in strategies between retail banking and other segments.

The evolution of segmentation toward more dynamic models that make it possible to act according to each customer’s moment and context.

Exploring how tools such as the NBA Decision Engine offered by Latinia enable real time event based activation.

Identify opportunities and challenges that this strategy presents.

We invite you to join us on this strategic journey, during which we will unveil key insights and approaches that will enable us to fine-tune our segmentation tactics in today’s banking landscape.

Customer Segmentation in Retail Banking vs. Other Segments

The banking world is diverse and complex, encompassing a wide range of services and clients. Each type of banking has its specific customer typology and, therefore, its own strategies and methods for bank customer segmentation. Below, we briefly describe the types of banking and their segmentation at a high level:

Retail Banking: Serves individual consumers and offers essential banking services like savings accounts, checking accounts, and consumer loans.

Private Banking: Focuses on high-net-worth individuals and provides personalized wealth management and financial advisory services.

Commercial Banking: Targets small to medium-sized businesses and provides business loans, cash management, and other business-related financial services.

Wholesale Banking: Works with large corporations, financial institutions, and governments, offering services like project financing and debt issuance.

Investment Banking: Caters to corporate clients and high-net-worth individuals, specializing in capital markets, mergers and acquisitions, and advisory services.

While each type of banking has its own segmentation and strategies, this article will focus specifically on the characteristics of customer segmentation in Retail Banking.

Retail Banking: Detailed Customer Segmentation

Retail Banking is possibly the most familiar banking segment for most people, as it deals directly with the average consumer, offering various products and services used in everyday life.

As we will see in the following sections, customer segmentation in retail banking can address various variables, such as:

Demographics: Age, gender, income, occupation, etc.

Geography: Location, urbanization, climate, etc.

Psychographics: Personality, values, lifestyle, etc.

Behavior: Brand loyalty, usage rate, willingness to switch, etc.

Applying these segmentation variables allows retail banks to design products, offers, and communication strategies that closely align with the needs and preferences of different customer groups.

Key Consumer Segments and Their Distinguishing Factors

Understanding key consumer segments and what sets them apart is vital for any bank aiming to nurture and expand customer relationships. Segmentation has become an indispensable tool that categorizes customers into subgroups based on various variables such as attitudes, needs, or behaviors.

Emerging customer profiles in modern banking

According to recent findings from CRIF and Accenture, today’s banking environment can be described through five clear customer profiles. These profiles reflect how preferences, expectations, and behaviours have shifted in a context where digital usage, trust, and advice now influence banking decisions more than ever.

1. The Digital First Customer

The preference for digital channels is growing consistently across all age groups.

42% avoid calling the bank and prefer chat or digital interaction – CRIF

Digital banks already capture a large share of the market and that customers maintain relationships with two banks and two digital wallets on average.

Profile characteristics:

Uses the mobile phone as the main channel for all operations.

Values real time actions, fast decisions and frictionless processes.

Avoids phone or in person interactions whenever possible.

Demands fast, clear and always available experiences.

2. The Hybrid Digital Physical Customer

Although digital usage is rising, 78% still prefer to speak with a person when the decision is important, such as a loan or mortgage.

Many users “combine channels” and the mobile phone should act as the orchestrator, not as the only channel.

Profile characteristics:

Uses the app for quick operations but goes to a branch for complex decisions.

Maintains a preference for human interactions to solve problems.

Demands continuity across channels (not repeating information).

3. The Young Digital Customer (Gen Z and Millennials)

Younger customers are the most likely to change banks if the digital experience is not satisfactory.

17% among those aged 18 to 24 would change their bank for a better digital experience. – CRIF

These generations are very open to using digital financial assistants, with 62% willing to use an artificial intelligence assistant to manage their finances.

Profile characteristics:

Demands real personalisation, not generic messages.

Seeks financial education: 88% want to learn more about finance.

Changes banks easily if they perceive a lack of transparency or complexity.

Views banking as a fully digitalisable, utilitarian service.

4. The Trust and Security Focused Customer

Concerns about privacy and data security are decisive.

62% of customers would leave a bank if they feel their data is not safe. – CRIF

Accenture confirms that 84% worry about how their information is used and have doubts about the use of artificial intelligence in financial services.

Profile characteristics:

Values the bank’s stability more than the digital experience.

Requires transparency in decisions and recommendations.

Needs explicit guarantees on data use and privacy.

5. The Advice Driven Customer (Decision Support Seeker)

Customers demand an approach where the bank “advises first, sells later”, especially for complex decisions.

82% of customers believe banks should help them avoid debt and make better decisions. – CRIF

Profile characteristics:

Seeks continuous guidance, not just products.

Wants to feel that the bank understands their personal situation.

Prefers tailored and transparent recommendations.

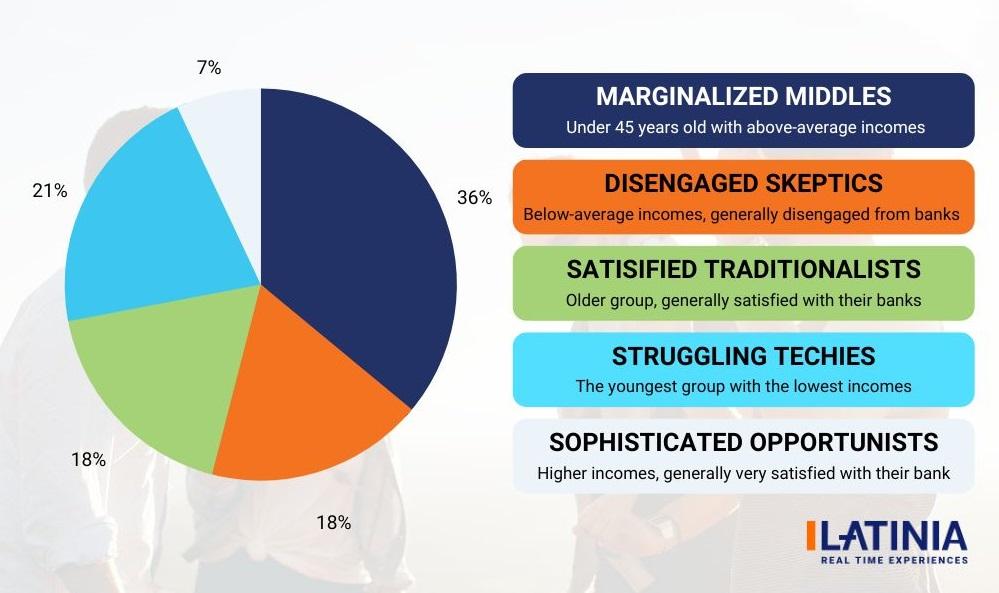

A Case Study: BAI and Cognizant

BAI and Cognizant conducted a detailed study focused on consumers of financial institutions in the United States. They identified five key segments, each with specific needs and behaviors:

Profile characteristics:

Marginalized Middles: Despite being the largest segment, consisting of individuals under 45 years old with above-average incomes, they are less satisfied and more confused about banking fees. Effective strategies for this group could include clear and transparent marketing messages, especially regarding fees.

DisengagedSkeptics: This group, with below-average incomes, is generally disengaged from banks and uses their services less, especially mobile. Other banks could attract these dissatisfied consumers with similarly priced products and improved customer service.

Satisfied Traditionalists: Although generally satisfied with their banks, this older group is not particularly inclined to consolidate their products at a single institution and rarely uses digital services. Offering a wide variety of products could be an effective strategy here.

Struggling Techies: The youngest group with the lowest incomes is at a life stage with very low potential deposit income. However, they are willing to adopt new technologies and manage their finances, and are open to proactive offers from financial institutions.

Sophisticated Opportunists: This segment has an average age and higher incomes and is generally very satisfied with their primary financial institution. Understanding and meeting their needs through innovative tools and products can be fundamental, as they have the highest potential for deposit income per household.

While these segments provide a helpful perspective, it is crucial to understand that they represent a snapshot of a particular market at a specific time.

Source: BAI Research Study: The New Dynamics of Consumer Banking Relationships

The validity and applicability of these segments can vary, and each bank must conduct its own market research and segmentation, especially because consumer needs and behaviors evolve over time and can differ significantly between markets.

Other Segmentation Approaches

A more basic segmentation approach could be more demographic and based on life stages or professions, which may include but is not limited to:

Young Adults: Focusing on building their financial lives, possibly new to credit management and savings.

Professionals and Workers: Seeking convenient and efficient banking solutions to manage their daily income and expenses.

Retirees/Seniors: Possibly focusing on wealth management and ensuring a comfortable retirement.

Entrepreneurs and Business Owners: Seeking scalable and flexible financial solutions to manage and expand their businesses.

These segments also present diverse needs and expectations, so it is crucial for banks to thoroughly research and understand them, adapting their services and communications accordingly.

Developing and refining customer segmentation, based on existing studies and the bank’s internal data and market context, will be crucial to ensure that strategies, products, and services align with consumers’ changing needs, behaviors, and expectations.

Applying Customer Segmentation to Empower Banking Strategies

Customer segmentation is not just a theoretical strategy but a practice that, when efficiently applied, can lead to beneficial business tactics.

Effective segmentation enables banks to reach their customers more personally and meaningfully by aligning products, communications, and services with each segment’s specific needs and behaviors.

Let’s explore how segmentation can trigger concrete strategies in different areas of the banking sector.

Designing Personalized Products and Services

Understanding different customer segments’ desires, behaviors, and needs allows financial institutions to develop and offer products and services tailored specifically to each group’s characteristics.

Product Development: Based on the peculiarities of each segment, the bank can create customized products. For example, for “Struggling Techies,” who are more inclined toward digital services, a bank could develop mobile applications with intuitive user interfaces and simplified transaction processes.

Additional Services: Providing additional services such as virtual financial advisory for “Sophisticated Opportunists” or educational programs on personal finance for “Young Adults.”

Pricing Models: Establishing pricing structures and fees that align with the expectations and capabilities of each segment, such as offering fee-free accounts for younger segments or premium services for higher-income segments.

Personalized Communication: Using segment data to create messages that speak directly to the needs and desires of customers, such as emails or in-app notifications highlighting products or offers that are genuinely relevant to them.

Offers and Promotions: Developing promotions that directly appeal to target segments. This could involve special offers for new customers in a particular segment or discounts on services popular among specific groups.

Targeted Advertising: Employing online advertising platforms to deliver ads specifically to defined user segments, thus maximizing the return on investment in advertising.

Enhancing the Customer Experience

A positive customer experience is crucial for customer loyalty and, consequently, for the success of the banking business.

Customer Journey: Analyzing the various ways different segments interact with banking services, banks can optimize the customer journey to make it as intuitive and frictionless as possible.

Support and Customer Service: Tailoring support and communication channels for each segment. While some may prefer virtual assistance, others may value a more personal and direct approach.

Platforms and Channels: Customizing digital platforms to meet the expectations of different segments, ensuring that the most relevant functionalities and information are easily accessible to each group.

“In today’s banking environment, if you’re speaking to everyone, you’re not speaking to anyone. Real relevance doesn’t come from having many products, but from offering the right product to the right person at the right moment.”

A Practical Framework: Implementing Customer Segmentation in 4 Steps

Moving from theory to execution is where segmentation truly delivers value. While many industry reports describe what segmentation is, few explain how banks can operationalize it. The following four step framework offers a clear and actionable way to bring segmentation to life inside a financial institution.

Step 1: Data Collection and Analysis

Effective segmentation starts with high quality data. Banks must gather and unify information from transactional activity, digital behavior, product usage, and customer interactions across channels. This stage also requires responsible data management practices, including clear handling policies and alignment with privacy regulations such as GDPR. The goal is to build a reliable data foundation that enables accurate insights into customer needs, preferences, and intentions.

Step 2: Defining Segments and Customer Personas

Once the data is organized, the next step is identifying meaningful groups. Banks can classify customers based on demographic attributes, behaviors, financial goals, life stages, or levels of digital engagement. From these clusters, institutions can build detailed personas that represent the motivations, challenges, and expectations of each segment. Well defined personas help teams design relevant products, messages, and service models.

Step 3: Activating Communication with the Right Action

Communication only becomes impactful when it drives action. This requires using technology to deliver the right product, message, or notification at the exact moment the customer needs it. Here is where real time decision engines play a decisive role. The Real-time Decition Engine of Latinia naturally fits into this step by analyzing customer events and transactions in real time and determining the most relevant next best action for each individual. This ensures that communication is not static, but continuously activated through context aware interactions.

Step 4: Measuring Success with KPIs

No segmentation strategy is complete without proper measurement. Banks should track the performance of each segment through key indicators such as Customer Lifetime Value, churn rate, product adoption, or engagement with personalized messages. Monitoring these KPIs allows institutions to refine their segmentation model, identify friction points, and adjust offerings to maximize business impact.

Expert tip: The real value lies in the moment

Segmentation helps you understand who the customer is, but the real opportunity appears when the bank detects an event that shows what the customer is experiencing right now. What truly makes a difference is not classifying, but responding at the right moment with a useful and contextual action.

From customer segmentation to event driven activation

Customer segmentation remains a valuable tool to understand profiles and behavior patterns. It helps identify groups, anticipate interests and plan strategies with a broad view. However, segmentation usually ends up in scheduled campaigns sent at times defined by the bank: a date, a time or a preset flow.

That means communication depends more on the timing designed by the institution than on what the customer is actually experiencing at that moment. Segmentation describes who the customer is, but not necessarily what they are doingnow or whether it is the right moment to act.

A logic focused on events and context

Most customers spend very few minutes a day on digital banking. That limited time makes it difficult to reach them through scheduled campaigns or segmentations that rely on their navigation. This raises an unavoidable question: how can you act if the user is barely present?

This is where context becomes meaningful.

Every interaction, such as a failed payment, an unusual login or a one time withdrawal, happens at a specific moment and generates information that helps understand what the customer is experiencing.

To respond appropriately to that moment, the bank needs technology able to detect those events in real time and decide whether it makes sense to act. Latinia’s RTD engine plays that role: instead of trying to anticipate behavior through static flows, the bank accompanies the customer based on what they are experiencing right then.

Contextual activation with Next Best Actions

Next Best Actions identify the moment when something relevant happens in the customer’s life and determine the most appropriate action for that moment.

Latinia’s NBA Decision Engine analyzes events and their associated data to select the most useful content and deliver it through the most suitable available channel.

Each NBA rule can be configured without additional development and includes a saturation system that prevents the customer from receiving more messages than necessary. This helps maintain trust and ensures a carefully managed experience.

Additional Resource: Implementing Next Best Actions Successfully

To help banking teams put NBAs into practice, Latinia offers a free guide focused on building, executing, and optimizing NBA strategies.

In this guide, you will learn how to:

Strengthen customer relationships through NBA driven strategies.

Define relevant NBAs and identify the right moments using transactional and geolocated events.

Apply best practices to avoid intrusive communications and use the right channels securely.

Improve conversion and increase sales of banking products.

Leverage Latinia NBA to deploy an NBA strategy easily and with full real time capabilities.

Measuring ROI: The KPIs That Matter in the Banking Sector

To assess whether a segmentation strategy is truly driving business impact, banks need to monitor the right performance indicators. These KPIs reveal how effectively each segment contributes to growth, profitability, and long term customer value.

Customer Lifetime Value (CLV)

CLV helps determine the long term revenue potential of each segment. By understanding which groups generate higher value over time, banks can prioritize investments, personalize offers more efficiently, and allocate resources where they have the greatest impact.

Customer Churn Rate

Churn indicates how many customers are leaving the bank and how segmentation can help retain them. Identifying which segments show early signs of attrition allows teams to take timely actions that strengthen loyalty and reduce revenue loss.

Product Penetration Rate

This KPI measures how many products customers in each segment are using. Higher penetration reflects stronger relationships, better cross selling, and deeper engagement. Tracking these metric highlights opportunities to increase adoption and design more relevant product bundles.

Final Insights into Customer Segmentation in Banking

Customer segmentation in the banking sector is not merely a marketing strategy; it is essential for the effective and efficient delivery of financial products and services. The correct identification and analysis of different customer groups allow banks to personalize their offerings, optimize their operations, and maximize profitability.

As a sector that impacts almost every other sector of the economy, banking significantly benefits from understanding and anticipating its customers’ needs through effective segmentation.

Strategies for the Future and the Evolution of Customer Segmentation

Looking to the future, banking will face emerging challenges and opportunities in customer segmentation. The accelerated adoption of digital technologies, shifts in customer preferences, and the evolution of the regulatory environment will be crucial factors influencing customer segmentation strategies.

The use of artificial intelligence, machine learning, and predictive analytics will become even more prevalent and sophisticated, enabling deeper and more dynamic segmentation and personalization. Additionally, customer expectations for personalized and frictionless banking experiences will continue to grow, driving banks toward continuous innovations in their segmentation strategies and product/service delivery.

Considerations and Next Steps for Banking Professionals

For banking professionals looking to make the most of customer segmentation opportunities, the following steps and considerations can be crucial:

Technology Adoption: Embrace and maximize the use of emerging technologies, such as real-time analysis and decision engines, to enhance the accuracy and effectiveness of customer segmentation.

Customer-Centricity: Ensure that segmentation strategies and resulting offerings are genuinely aligned with customer needs and desires.

Strategic Agility: Develop the ability to quickly adapt segmentation strategies to changes in the market and customer behavior.

Regulatory Compliance: Ensure that segmentation strategies and implementation tactics comply with relevant local and international regulations.

Continuous Innovation: Foster a culture of constant innovation to anticipate emerging customer needs and stay competitive in the market.

Ongoing Training: Ensure teams have the necessary skills and knowledge to effectively interpret and act on segmentation data.

Conclusion

Ultimately, customer segmentation will be a fundamental strategic pillar in the future of banking, providing institutions with the necessary tools and insights to serve their customers optimally and navigate successfully in a constantly evolving financial landscape.

Banks that can integrate effective segmentation strategies with advanced technology and customer-centric execution will be optimally positioned to succeed in the future of the financial sector.

If you want to learn more about how Latinia can integrate into your customer experience strategy, don’t hesitate to contact us. Our team of experts is ready to advise you on your journey toward a more personalized, secure, and customer-oriented banking service where every interaction counts in building stronger and lasting relationships.

Frequently Asked Questions about Customer Segmentation for Banks

What are the most common types of customer segmentation in banks?

How does technology help in bank customer segmentation?

Technology makes it possible to identify customer groups with much greater accuracy through large scale data analysis, artificial intelligence and machine learning. These capabilities help reveal patterns, anticipate interests and fine tune the offer.

It has also enabled a further step. It is no longer just about segmenting, but about acting at the exact moment something relevant happens to the customer. Real time decision solutions such as Latinia’s RTD Engine detect events as they occur and assess whether it is the right moment to respond.

Why is customer segmentation important in the banking sector?

Segmentation helps banks deliver more relevant products, reveal patterns, improve customer retention, and increase profitability. By understanding the specific needs and behaviors of each segment, banks can design better experiences, strengthen relationships, and optimize business performance.

In banking, customer segmentation is more than just a tool; it's the central strategy for effectively connecting with our users and their needs. Each customer, with their unique demands and financial…

In banking, customer segmentation is more than just a tool; it's the central strategy for effectively connecting with our users and their needs. Each customer, with their unique demands and financial…

In banking, customer segmentation is more than just a tool; it's the central strategy for effectively connecting with our users and their needs. Each customer, with their unique demands and financial…

In banking, customer segmentation is more than just a tool; it's the central strategy for effectively connecting with our users and their needs. Each customer, with their unique demands and financial…

In banking, customer segmentation is more than just a tool; it's the central strategy for effectively connecting with our users and their needs. Each customer, with their unique demands and financial…

In banking, customer segmentation is more than just a tool; it's the central strategy for effectively connecting with our users and their needs. Each customer, with their unique demands and financial…

In banking, customer segmentation is more than just a tool; it's the central strategy for effectively connecting with our users and their needs. Each customer, with their unique demands and financial…

In banking, customer segmentation is more than just a tool; it's the central strategy for effectively connecting with our users and their needs. Each customer, with their unique demands and financial…

In banking, customer segmentation is more than just a tool; it's the central strategy for effectively connecting with our users and their needs. Each customer, with their unique demands and financial…

In banking, customer segmentation is more than just a tool; it's the central strategy for effectively connecting with our users and their needs. Each customer, with their unique demands and financial…

In banking, customer segmentation is more than just a tool; it's the central strategy for effectively connecting with our users and their needs. Each customer, with their unique demands and financial…

In banking, customer segmentation is more than just a tool; it's the central strategy for effectively connecting with our users and their needs. Each customer, with their unique demands and financial…

Para ofrecer las mejores experiencias, utilizamos tecnologías como las cookies para almacenar y/o acceder a la información del dispositivo. El consentimiento de estas tecnologías nos permitirá procesar datos como el comportamiento de navegación o las identificaciones únicas en este sitio. No consentir o retirar el consentimiento, puede afectar negativamente a ciertas características y funciones.

Funcional

Always active

El almacenamiento o acceso técnico es estrictamente necesario para el propósito legítimo de permitir el uso de un servicio específico explícitamente solicitado por el abonado o usuario, o con el único propósito de llevar a cabo la transmisión de una comunicación a través de una red de comunicaciones electrónicas.

Preferencias

El almacenamiento o acceso técnico es necesario para la finalidad legítima de almacenar preferencias no solicitadas por el abonado o usuario.

Estadísticas

El almacenamiento o acceso técnico que es utilizado exclusivamente con fines estadísticos.El almacenamiento o acceso técnico que se utiliza exclusivamente con fines estadísticos anónimos. Sin un requerimiento, el cumplimiento voluntario por parte de tu proveedor de servicios de Internet, o los registros adicionales de un tercero, la información almacenada o recuperada sólo para este propósito no se puede utilizar para identificarte.

Marketing

El almacenamiento o acceso técnico es necesario para crear perfiles de usuario para enviar publicidad, o para rastrear al usuario en una web o en varias web con fines de marketing similares.