Instant Payments in North America: Current systems and future developments

Latinia

•29 de January de 2025•6 min read

In North America, instant payment systems are rapidly evolving, driven by technological advancements and regulatory initiatives aimed at accelerating transaction processing and enhancing financial ecosystems. This progress not only improves efficiency but also positions account-to-account transfers as one of the most significant trends in digital payments for 2024.

These developments have opened new opportunities for banks and fintech companies striving to build sustainable business models aligned with regulatory frameworks in the region.

In this landscape, the U.S. already has well-established real-time payment networks, while Canada is in the process of implementing its own solutions to modernize financial transactions. Below, we analyze the main instant payment systems currently in place and the key technologies supporting their development.

Instant Payment Systems in the U.S

The U.S. has made significant strides in developing instant payment systems, driven by the demand for faster and more efficient transactions. With solutions that enable real-time transfers between financial institutions, businesses, and consumers, the country now has multiple platforms designed to improve liquidity and streamline digital payments.

The FedNow Service

Launched by the Federal Reserve in July 2023, the FedNow Service is a real-time payment infrastructure designed to enable instant transactions between financial institutions across the U.S. Unlike traditional payment systems, which may take hours or even days to process transactions, FedNow operates 24/7/365, ensuring that businesses and individuals can send and receive funds immediately, improving cash flow and financial flexibility.

Financial institutions of all sizes can participate in the service, allowing them to offer instant payment capabilities to their customers. This makes FedNow particularly useful for account-to-account (A2A) transfers, bill payments, and other time-sensitive transactions. Additionally, service providers can leverage this infrastructure to build innovative financial solutions that take advantage of real-time payments.

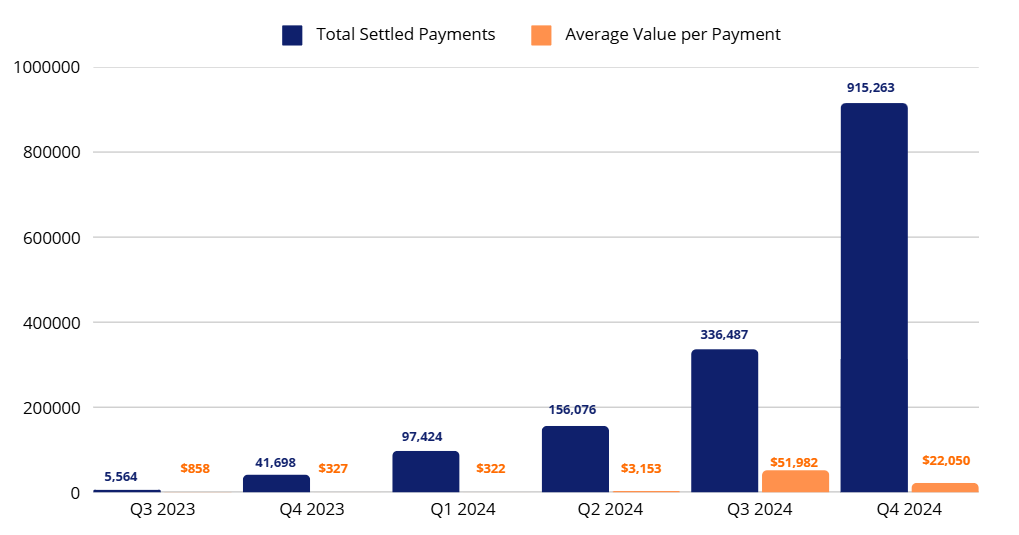

According to the Federal Reserve, since 2023, FedNow has experienced explosive growth in both transaction volume and value:

Total transactions2024: Over 1.5 million, a 2,097% increase from 2023.

Total value of payments2024: Nearly $38 billion, up 147,600% from 2023.

Average transaction size: Grew from $327 in late 2023 to over $22,000 in 2024, indicating a shift toward larger, business-oriented payments.

This rapid adoption reflects the growing importance of real-time payments in the U.S. financial ecosystem. As more banks and businesses integrate FedNow, it is set to become a cornerstone of instant payments, reducing settlement delays and improving cash flow management.

The RTP Network

Launched in 2017 by The Clearing House, the RTP (Real-Time Payments) Network was the first real-time payment system in the U.S. It enables instant fund transfers, allowing consumers, businesses, and government entities to send and receive money immediately through participating financial institutions.

The RTP network is open to all insured U.S. depository institutions, and financial entities can integrate either directly or through third-party service providers, such as corporate credit unions and bankers’ banks. This flexibility has contributed to its broad adoption, allowing it to reach 70% of U.S. demand deposit accounts (DDAs), with an extended technical reach to institutions holding nearly 90% of DDAs.

According to The Clearing House, by 2024, the RTP network processed 87 million transactions valued at $69 billion, reflecting its increasing role in modernizing real-time payments. The average daily volume now surpasses 1 million transactions, with a total daily value of $771.7 million. Over 750 financial institutions actively use RTP, ensuring that real-time payme

Zelle: Peer-to-Peer Instant Transfers

Zelle is one of the most widely used instant payment services in the U.S., enabling peer-to-peer (P2P) transactions between individuals and small businesses. Unlike FedNow and the RTP network, which operate as payment infrastructures, Zelle functions as a consumer-facing service integrated into banking apps, allowing users to send money instantly using just a phone number or email address.

According to Zelle, it has seen remarkable growth, with 120 million consumer and small business accounts using the service in 2023. Over the past year, transaction volume increased by 28%, with users sending 2.9 billion transactions totaling $806 billion.

Small businesses have significantly increased their use of Zelle, receiving 217 million payments worth over $100 billion in 2023. On the sending side, small businesses processed 179 million payments totaling $113 billion, reflecting 34% and 29% year-over-year growth. This highlights Zelle’s expanding role beyond P2P transfers, becoming a key tool for business payments, including paying vendors, employees, and rent.

Instant Payment Systems in Canada

Canada is actively modernizing its payment ecosystem to enhance transaction speed, security, and accessibility. While Interac e-Transfer has long been the dominant platform for fast payments, the country is preparing for a major shift with the development of Real-Time Rail (RTR), a national instant payment infrastructure set to launch in 2026.

Real-Time Rail (RTR)

Canada’s Real-Time Rail (RTR) is a new instant payment system designed to make transactions faster, more secure, and data-rich across the country. Managed by Payments Canada, RTR will enable 24/7 real-time payments, ensuring that funds are sent, received, cleared, and settled instantly.

Originally planned for 2023, its launch has been delayed to 2026 due to the complexity of building a secure and resilient payment infrastructure. Once live, RTR will support a wide range of transactions, including P2P, B2B, and G2C payments, making it useful for individuals, businesses, and government entities alike.

One of its key features is advanced fraud prevention, providing an extra layer of security to protect users. Additionally, RTR will use the ISO 20022 standard, allowing transactions to carry more detailed data, improving transparency and efficiency.

With its launch, RTR is set to modernize Canada’s payment landscape, offering faster, safer, and more efficient payment solutions for everyday transactions.

Interac e-Transfer

Launched in 2021, Interac e-Transfer is Canada’s most widely used instant payment system, enabling individuals and businesses to send and receive money using just an email or phone number, with transactions processed within minutes, 24/7.

Unlike the upcoming Real-Time Rail (RTR), Interac e-Transfer relies on existing banking infrastructure, meaning payments are fast but not always real-time. RTR will also support larger transactions, including B2B and government payments, while Interac e-Transfer is mainly used for P2P, small business, and bill payments.

According to Interac and data from the Bank of Canada, in 2023, 88% of Canadian adults used Interac e-Transfer, with 61% making monthly transactions. The total transaction volume reached$383 billion, and businesses sent 26 million payments, averaging 19.5 per employer in Canada.

Key technologies for instant payment systems

The implementation of instant payment systems requires advanced technologies that ensure security, immediacy, and trust. Some of the most important ones include:

Real-time notifications keep users informed of any transaction instantly, improving their confidence and security.

Transactional data analysis identifies suspicious patterns and behaviors in real time, generating alerts to prevent fraud and optimize customer communication.

A reliable notification delivery system ensures that critical messages, such as authorizations or fraud alerts, reach users without failures, protecting both the customer and the financial ecosystem.

One of the best ways to strengthen instant payment systems is by integrating advanced solutions like those offered by Latinia. Our technology, based on real-time transactional data analysis, allows immediate notification of any activity to the customer. This instant communication enables quick confirmation or rejection of operations, significantly reducing fraud risks.

Additionally, our Critical Event Gateway system ensures that critical messages are delivered reliably and without delay.

Whether it’s fraud suspicion alerts, OTP authorizations, or other important notifications, this system guarantees swift customer responses, strengthening trust and effectively protecting the financial ecosystem.

Discover how Latinia’s real-time communication solutions help improve customer satisfaction and fraud prevention for your bank’s instant payment system. Contact us for a consultation and visit our website for more details.

In North America, instant payment systems are rapidly evolving, driven by technological advancements and regulatory initiatives aimed at accelerating transaction processing and enhancing financial…

In North America, instant payment systems are rapidly evolving, driven by technological advancements and regulatory initiatives aimed at accelerating transaction processing and enhancing financial…

In North America, instant payment systems are rapidly evolving, driven by technological advancements and regulatory initiatives aimed at accelerating transaction processing and enhancing financial…

In North America, instant payment systems are rapidly evolving, driven by technological advancements and regulatory initiatives aimed at accelerating transaction processing and enhancing financial…

In North America, instant payment systems are rapidly evolving, driven by technological advancements and regulatory initiatives aimed at accelerating transaction processing and enhancing financial…

In North America, instant payment systems are rapidly evolving, driven by technological advancements and regulatory initiatives aimed at accelerating transaction processing and enhancing financial…

In North America, instant payment systems are rapidly evolving, driven by technological advancements and regulatory initiatives aimed at accelerating transaction processing and enhancing financial…

In North America, instant payment systems are rapidly evolving, driven by technological advancements and regulatory initiatives aimed at accelerating transaction processing and enhancing financial…

In North America, instant payment systems are rapidly evolving, driven by technological advancements and regulatory initiatives aimed at accelerating transaction processing and enhancing financial…

In North America, instant payment systems are rapidly evolving, driven by technological advancements and regulatory initiatives aimed at accelerating transaction processing and enhancing financial…

In North America, instant payment systems are rapidly evolving, driven by technological advancements and regulatory initiatives aimed at accelerating transaction processing and enhancing financial…

Para ofrecer las mejores experiencias, utilizamos tecnologías como las cookies para almacenar y/o acceder a la información del dispositivo. El consentimiento de estas tecnologías nos permitirá procesar datos como el comportamiento de navegación o las identificaciones únicas en este sitio. No consentir o retirar el consentimiento, puede afectar negativamente a ciertas características y funciones.

Funcional

Always active

El almacenamiento o acceso técnico es estrictamente necesario para el propósito legítimo de permitir el uso de un servicio específico explícitamente solicitado por el abonado o usuario, o con el único propósito de llevar a cabo la transmisión de una comunicación a través de una red de comunicaciones electrónicas.

Preferencias

El almacenamiento o acceso técnico es necesario para la finalidad legítima de almacenar preferencias no solicitadas por el abonado o usuario.

Estadísticas

El almacenamiento o acceso técnico que es utilizado exclusivamente con fines estadísticos.El almacenamiento o acceso técnico que se utiliza exclusivamente con fines estadísticos anónimos. Sin un requerimiento, el cumplimiento voluntario por parte de tu proveedor de servicios de Internet, o los registros adicionales de un tercero, la información almacenada o recuperada sólo para este propósito no se puede utilizar para identificarte.

Marketing

El almacenamiento o acceso técnico es necesario para crear perfiles de usuario para enviar publicidad, o para rastrear al usuario en una web o en varias web con fines de marketing similares.