Banking cybersecurity: Global challenges and strategic responses

Latinia

•15 de April de 2025•6 min read

Banks have always had a key advantage over many of their newer competitors — from fintech startups to big tech giants: customer trust. For decades, they’ve built strong relationships grounded in security, expertise, and regulatory compliance. But over the past 15 years, that trust has come under growing pressure because of the rapid growth of digital channels, the rise in banking fraud, and increasingly sophisticated cyberattacks.

Today, earning and protecting customer trust isn’t just about having solid internal processes — it requires real-time, customer-focused cybersecurity strategies that can adapt to a complex and evolving threat landscape.

It is no longer just about reacting to incidents, but about anticipating them through proactive, automated, and real-time strategies.

In this article, we take a closer look at the challenges facing banking cybersecurity— and the strategic responses helping financial institutions stay ahead.

The Current State of Cybersecurity in Banking

Cybersecurity has become one of the top concerns for the banking industry worldwide. The number of attacks is not only growing — they’re also becoming more complex, fueled by technologies like artificial intelligence and new tactics such as advanced phishing and vishing.

Europe: According to EY, 82% of Chief Risk Officers view cybersecurity as the top threat to their business in 2024. On a consumer level, 34% of citizens have been targeted by cyber threats, with phishing being the most common, affecting 26%, according to EUROSTAT.

Latin America: Financial institutions in the region are 300 times more likely to be targeted by cyberattacks compared to other industries, according to Fintech Americas. In response, average annual investment in cybersecurity has reached $18.5 million — 40% more than in other sectors.

United States: According to a CrowdStrike report, 71% of financial institutions have seen a rise in destructive cyberattacks. In 2024 alone, there were over 4,480 interactive intrusions. Notably, 79% of these attacks were “malware-free,” relying instead on tactics like credential abuse and social engineering.

This landscape aligns with what many industry experts have highlighted: the combination of digitalization, interconnected systems, and increasingly sophisticated attack methods is reshaping the risk landscape in banking, forcing institutions to adopt more integrated and proactive security approaches.

Key Cybersecurity Risks in Banking

Beyond the overall increase in cyberattacks, the banking sector faces a number of specific risks that make it a particularly attractive target for cybercriminals.

As noted by Marius Scarlat of Stefanini Group, factors such as accelerated digitalization, outdated systems, and growing third-party interconnectedness are increasing risk exposure across the financial sector.

Key risk factors include:

Legacy systems and technological obsolescence, which make it difficult to implement modern security layers and may contain unresolved vulnerabilities.

Third-party interconnectedness, particularly in open banking environments, where APIs and external providers expand the attack surface.

Mobile application vulnerabilities, as mobile banking continues to grow in popularity and security standards vary significantly across applications.

Social engineering and compromised credentials, which allow attackers to gain access without deploying malware by exploiting human behavior.

Combined with the vast amounts of sensitive data managed by financial institutions, these factors make cybersecurity not only a technological challenge but also a strategic one.

Key Strategies to Strengthen Cybersecurity in Banking

Reacting to threats is no longer enough. Financial institutions need to take a proactive approach — one that anticipates risks before they materialize.

Protecting against banking fraud means staying ahead of threats, embedding security into everyday decision-making, and reinforcing every layer of the organization — not just its technology.

The ability to monitor, analyze, and act in real time has become a critical differentiator for preventing threats before they become incidents.

Multi-Factor Authentication and Biometrics

One of the most effective ways to protect access to digital banking services is by establishing strong security barriers from the very first step.

Multi-factor authentication (MFA) strengthens this initial line of defense by requiring two or more forms of verification. This significantly reduces the risk of unauthorized access — even if a credential has been compromised.

Biometric verification systems also play a key role, allowing users to authenticate themselves accurately and seamlessly.

Implementing these mechanisms — along with robust identity verification practices like the Know Your Customer (KYC) model — helps prevent fraud related to identity theft or impersonation.

Beyond their technical impact, these measures also increase customers’ perception of security — especially during high-risk transactions or when accessing services from mobile devices. The challenge lies in striking the right balance between protection and user experience.

Continuous Monitoring and Real-Time Analysis

Spotting a threat in time can be the difference between a simple alert and a high-impact security incident. That’s why the ability to continuously monitor system activity has become essential.

Fraud detection algorithms powered by machine learning analyze large volumes of transaction data to identify patterns that may signal suspicious behavior. This allows banks to detect threats more accurately and earlier than ever before.

Real-time transaction monitoring enables the immediate detection of unusual activity, making it possible to respond instantly and drastically reduce the window of opportunity for fraudsters.

These solutions don’t just improve response times — they also allow institutions to take preventive action before fraud occurs, helping strengthen customer trust in digital banking channels.

Internal Training and a Security-First Culture

Human error remains one of the most common entry points for cyberattacks. That’s why having well-trained teams and a collective mindset focused on security is just as important as having advanced technology.

Ongoing staff training helps employees recognize and neutralize common manipulation tactics — like phishing, pretexting, or social engineering. The better prepared teams are, the less likely they are to make mistakes that could compromise security.

Building a strong security awareness culture ensures that everyone in the organization — from operational staff to senior management — sees cybersecurity as a shared responsibility.

Clear procedures for responding to potential threats also help ensure a fast, coordinated reaction when suspicious behavior is detected or unusual communications are received.

Ultimately, making security part of everyday operations not only reduces the risk of incidents, but it also strengthens the organization’s ability to anticipate and respond to future threats.

Alongside internal training, another increasingly important element is customer education. Awareness campaigns and clear communication about risks such as phishing and identity theft can significantly reduce exposure to fraud.

Collaboration with Institutions and Strategic Partnerships

Cybersecurity isn’t something banks can tackle alone. In an industry as connected as financial services, sharing information and working together is essential to stay ahead of new threats and respond faster when they happen.

Partnering with technology providers, fintechs, and other key players creates opportunities to share knowledge, adopt more flexible solutions, and build stronger defenses against common risks.

Being part of industry networks and specialized forums — like threat intelligence sharing centers — also helps banks stay on top of evolving attack tactics and emerging best practices.

Collaboration with regulators and government agencies is just as important. It ensures cybersecurity strategies stay aligned with evolving regulations and helps protect the stability of the financial system as a whole.

New regulations like the upcoming PSD3 in Europe are moving in that direction — promoting a more collaborative environment, enabling direct access to payment systems for new players, and encouraging real-time fraud information sharing across the industry.

The Critical Role of Customers in Banking Cybersecurity

In today’s environment, customers are not only users of digital financial services but also one of the primary targets of cyberattacks. Increasingly sophisticated social engineering techniques exploit common behaviors such as trusting seemingly legitimate communications or reusing credentials across services.

There is also a widespread perception of security that does not always reflect reality. While many users believe they can identify threats, attackers continuously evolve their tactics, increasing the likelihood of fraud.

This highlights a key reality: banking cybersecurity does not depend solely on technology. Customer behavior is a determining factor both in risk exposure and in the ability to respond to potential threats.

For this reason, financial institutions must integrate customers into their security strategies, not only as users to be protected, but as active participants in fraud detection and prevention.

Three key areas of action stand out:

Education and awareness, helping customers recognize fraud attempts, identify suspicious activity, and understand how to respond to potential attacks.

Implementation of security tools, such as multi-factor authentication, biometrics, and one-time passwords, to strengthen protection during access and transactions.

Customer engagement and empowerment, providing communication channels and control mechanisms that enable customers to react quickly when suspicious situations arise.

Integrating these elements allows banks to significantly reduce fraud risk and move toward a more collaborative security model, where customers and institutions work together to protect information and transactions.

The Economic Impact of Security Breaches in Banking

Security breaches affect not only customer trust but also business performance. According to the Cost of a Data Breach 2025 report by IBM Security and the Ponemon Institute, the global average cost of a data breach stands at $4.4 million. Although this figure has decreased compared to the previous year, it still reflects the magnitude of the challenge.

The report also highlights the growing role of artificial intelligence. On the one hand, organizations that make extensive use of AI in their security systems can significantly reduce the financial impact of breaches, achieving savings of up to $1.9 million compared to those that do not use AI.

However, this rapid adoption also introduces new risks. Among organizations reporting AI-related incidents, 97% lacked adequate access controls, while 63% had no governance policies in place to manage AI usage or prevent the spread of shadow AI.

This reinforces a key lesson: the combination of response speed, automation, and governance is crucial for reducing both the likelihood and the financial impact of security breaches.

Real-Time Communication Applied to Banking Cybersecurity

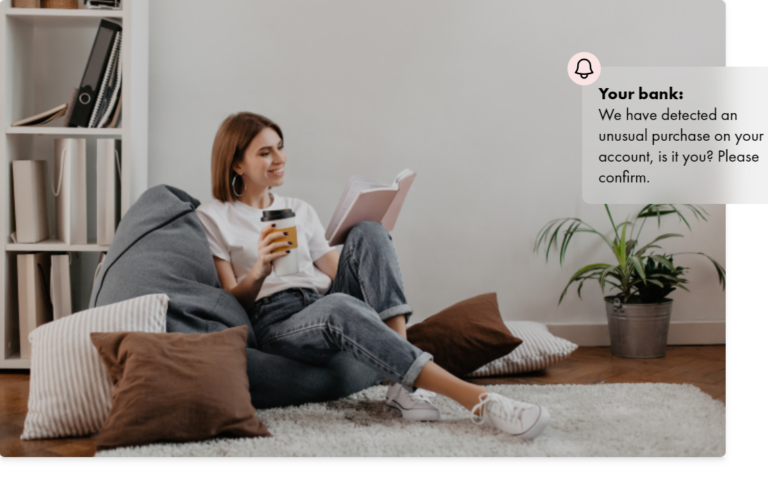

Real-time communication has become a cornerstone of modern banking security strategies. Instant notifications are now essential for early threat detection and fraud prevention.

In this context, the ability to communicate effectively with customers becomes a decisive factor. As María José Echevarría, Regional Sales Manager at Latinia, explains: “Improving communication with customers is a key element in the fight against cyberattacks. Real-time alert services, such as our decision engines specialized in filtering and analyzing transactional events in real time, can play a significant role in strengthening cybersecurity across the banking sector.”

In cybersecurity, timing is everything. If a critical alert reaches the customer too late, the system has already failed. True real-time communication happens in less than a second — that’s the window banks have to trigger alerts and connect with customers immediately.

For example, if there’s an unusually large transfer from a location the customer doesn’t normally use, the system can automatically send an SMS notification along with a one-time password (OTP) to authorize the transaction. If the customer doesn’t recognize the payment or doesn’t respond, the transaction can be blocked instantly.

This is where Latinia plays a key role — helping banks act with the speed and precision today’s environment demands:

Real-time transaction alerts based on rules configured from both historical and real-time transactional data — enabling banks to instantly notify customers about unusual activity and give them the ability to validate or block the operation.

Guaranteed message delivery through the Critical Event Gateway — a system that ensures critical messages like fraud alerts or OTP codes are delivered on time, even during peak traffic periods.

Customizable rule-based notifications that trigger alerts based on specific criteria like transaction amount, location, or frequency — helping banks strike the right balance between accuracy and relevance.

These capabilities allow financial institutions to automate their response to potential threats, meet the most demanding regulatory requirements, and — most importantly — strengthen customer trust. In the fight against fraud, speed of response makes all the difference.

Latinia is more than just an alert system — it’s a real-time decision and communication engine, built specifically for the needs of the banking industry. With deep expertise in the financial sector and seamless integration into existing systems, we help banks protect their customers at the exact moment they need it most.

Discover how Latinia’s real-time communication solutions can help strengthen your bank’s cybersecurity. Contact us for a consultation and visit our website to learn more.

Banks have always had a key advantage over many of their newer competitors — from fintech startups to big tech giants: customer trust. For decades, they’ve built strong relationships grounded in…

Banks have always had a key advantage over many of their newer competitors — from fintech startups to big tech giants: customer trust. For decades, they’ve built strong relationships grounded in…

Banks have always had a key advantage over many of their newer competitors — from fintech startups to big tech giants: customer trust. For decades, they’ve built strong relationships grounded in…

Banks have always had a key advantage over many of their newer competitors — from fintech startups to big tech giants: customer trust. For decades, they’ve built strong relationships grounded in…

Banks have always had a key advantage over many of their newer competitors — from fintech startups to big tech giants: customer trust. For decades, they’ve built strong relationships grounded in…

Banks have always had a key advantage over many of their newer competitors — from fintech startups to big tech giants: customer trust. For decades, they’ve built strong relationships grounded in…

Banks have always had a key advantage over many of their newer competitors — from fintech startups to big tech giants: customer trust. For decades, they’ve built strong relationships grounded in…

Banks have always had a key advantage over many of their newer competitors — from fintech startups to big tech giants: customer trust. For decades, they’ve built strong relationships grounded in…

Banks have always had a key advantage over many of their newer competitors — from fintech startups to big tech giants: customer trust. For decades, they’ve built strong relationships grounded in…

Banks have always had a key advantage over many of their newer competitors — from fintech startups to big tech giants: customer trust. For decades, they’ve built strong relationships grounded in…

Banks have always had a key advantage over many of their newer competitors — from fintech startups to big tech giants: customer trust. For decades, they’ve built strong relationships grounded in…

Banks have always had a key advantage over many of their newer competitors — from fintech startups to big tech giants: customer trust. For decades, they’ve built strong relationships grounded in…

Para ofrecer las mejores experiencias, utilizamos tecnologías como las cookies para almacenar y/o acceder a la información del dispositivo. El consentimiento de estas tecnologías nos permitirá procesar datos como el comportamiento de navegación o las identificaciones únicas en este sitio. No consentir o retirar el consentimiento, puede afectar negativamente a ciertas características y funciones.

Funcional

Always active

El almacenamiento o acceso técnico es estrictamente necesario para el propósito legítimo de permitir el uso de un servicio específico explícitamente solicitado por el abonado o usuario, o con el único propósito de llevar a cabo la transmisión de una comunicación a través de una red de comunicaciones electrónicas.

Preferencias

El almacenamiento o acceso técnico es necesario para la finalidad legítima de almacenar preferencias no solicitadas por el abonado o usuario.

Estadísticas

El almacenamiento o acceso técnico que es utilizado exclusivamente con fines estadísticos.El almacenamiento o acceso técnico que se utiliza exclusivamente con fines estadísticos anónimos. Sin un requerimiento, el cumplimiento voluntario por parte de tu proveedor de servicios de Internet, o los registros adicionales de un tercero, la información almacenada o recuperada sólo para este propósito no se puede utilizar para identificarte.

Marketing

El almacenamiento o acceso técnico es necesario para crear perfiles de usuario para enviar publicidad, o para rastrear al usuario en una web o en varias web con fines de marketing similares.