From Overload to Relevance: Strategies to Prevent Push Notification Fatigue

Latinia

•5 de September de 2025•6 min read

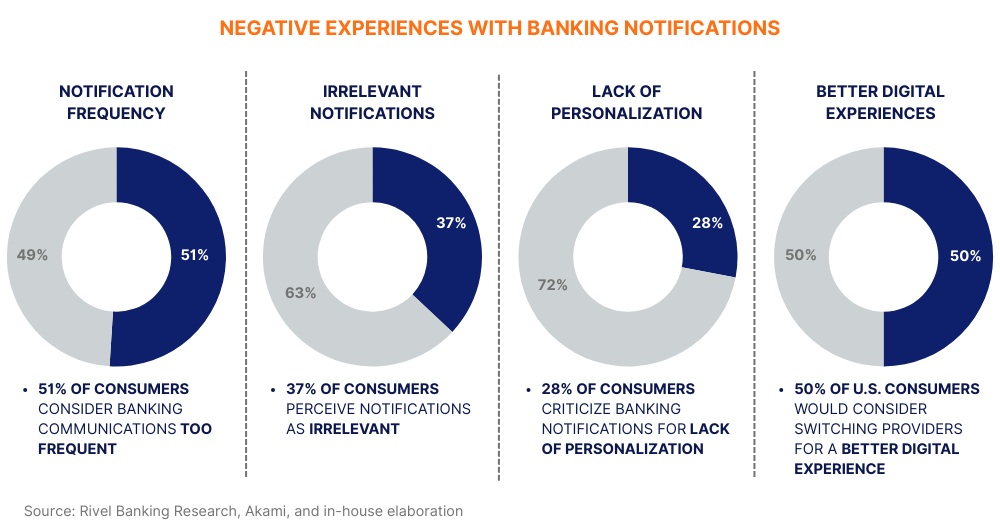

According to Reuters, 43% of users turn off alerts because they find them excessive or irrelevant. The rapid pace of digitalization has made push notifications a cornerstone of communication between banks and their customers.

But the rise of this channel brings a new challenge: how can banks stay relevant and avoid user fatigue in a world where mobile devices are constantly buzzing with alerts?

Growth of Push Notifications in Banking

The Rise of Mobile and the New Standard for Communication

Digital transformation in banking has placed mobile at the center, making smartphones the primary gateway to financial products and services. Back in 2024, when we released the Push Channel Trends Report, data already showed push notifications in banking growing at annual rates above 40% in key markets. This surge has been driven by the expansion of mobile infrastructure and the rising demand for fast, personalized digital experiences.

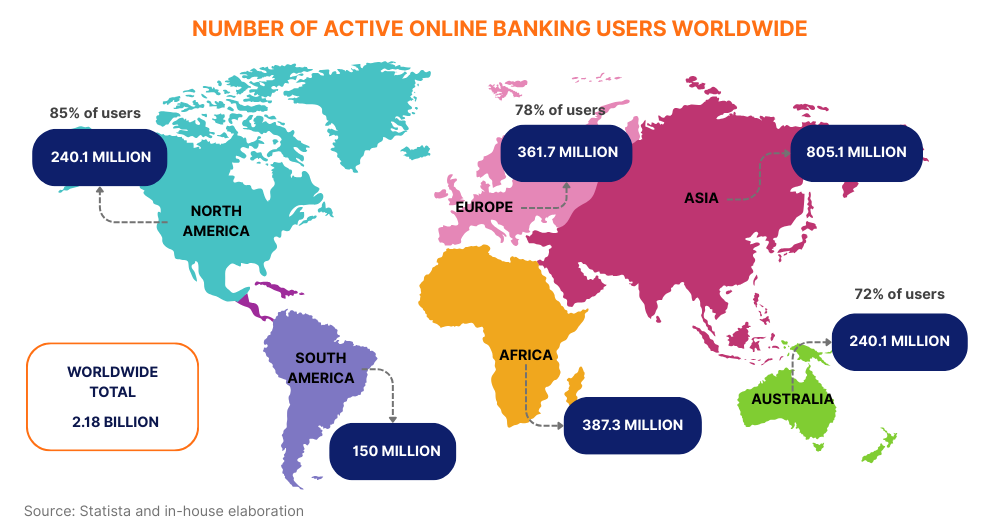

On a global scale, Europe has established itself as a leader in both digital maturity and banking regulation, with Nordic countries surpassing 95% penetration in online banking. Spain, with 71.45%, also sits above the European average of 63.87%, according to the 2024 Funcas Report. Still, leadership isn’t universal: Asia sets the pace with massive adoption of mobile financial services, Latin America stands out for its rapid growth in mobile-driven financial inclusion, and the United States remains a highly digitalized market, though less uniform than Europe or Asia. This context shows that Europe’s progress is not an isolated case, but part of a broader global shift toward digital and mobile banking.

This shift is also reflected in the growing preference for push notifications, which now account for up to 60% of digital banking interactions in key markets like Spain and Mexico. These figures highlight a global demand for agile, immediate, and personalized digital experiences that are redefining today’s standard for banking communication.

Demand for Immediacy and Rising Digital Expectations

Shifts in digital consumption habits have raised banking customers’ expectations to unprecedented levels. It’s no longer enough to provide a fast service—clients now expect real-time responses, instant updates on their transactions, and 24/7 communication without friction or interruptions.

In this context, push notifications have become a key resource. Their ability to deliver messages instantly, combined with a high degree of personalization, makes them the ideal channel to meet these demands: from account activity alerts and transfer confirmations to payment reminders, investment opportunities, pre-approved loans, or contextual recommendations based on customer behavior.

The Risk of Overload: Digital Fatigue and the Customer Experience

The omnipresence of notifications, if not carefully managed, poses a serious challenge. Customers can quickly shift from valuing timely information to feeling overwhelmed when the frequency or content of messages doesn’t match their actual needs. This is where notification fatigue comes in—a phenomenon widely studied across the fintech industry.

Excessive irrelevant notifications have clear consequences: lower open rates, higher opt-out rates, and reduced engagement. According to the Reuters Institute, 43% of users turn off alerts because they find them excessive or irrelevant.

The impact goes beyond engagement—reputation is also at stake. Poor notification experiences lead to negative reviews and customer churn, especially among digital natives.

This phenomenon even finds parallels in the field of security. MFA fatigue attacks exploit user overload by sending repeated authentication requests to trigger human error. The takeaway is clear: customer trust depends on striking the right balance between immediacy and relevance, where every notification addresses a real need rather than just adding to the volume of communication.

Strategies to Prevent Fatigue and Achieve Relevance: From Mass Messaging to Meaningful Personalization

Notification overload can be avoided with the right approach. Research and real-world experience show that banks shifting from indiscriminate messaging to personalized, contextual, and manageable communication achieve stronger loyalty, higher open rates, and fewer opt-outs.

According to McKinsey’s Global Banking Annual Review 2024, institutions that apply advanced real-time personalization achieve up to 30% more digital engagement and a 20% reduction in notification opt-outs compared to generic approaches.

Banks need to move beyond mass messaging and embrace advanced segmentation powered by analytics and machine learning.

Chase (U.S.) applies intelligent rules that determine not only which messages to send, but also the best channel and timing based on interaction history.

CaixaBank and BBVA (Europe) have implemented decision engines that adjust the type and frequency of alerts according to financial profiles, customer relationships, and usage context.

Nubank (LatAm) uses transactional and behavioral data to distinguish between critical alerts (e.g., fraud) and proactive recommendations (e.g., savings goals).

Banks must move past indiscriminate sending and commit to advanced segmentation supported by analytics and machine learning.

2. Contextualization and Artificial Intelligence: Timely, Relevant Messages

AI makes it possible to detect patterns and anticipate when a customer will truly value a notification. Context turns an alert into assistance rather than an intrusion:

HSBC triggers notifications when travel is detected, offering reminders about security and exchange rates.

Capital One (U.S.) uses AI to identify unusual spending and send personalized alerts within seconds.

Banco Industrial (Guatemala) worked with us at Latinia to modernize its communications by integrating real-time push and SMS notifications. This enabled the delivery of critical messages with average send times measured in tenths of a second and 9% service continuity—especially valuable in areas with limited connectivity.

When customers receive exactly what they need, at the moment they need it, and with the confidence that the message will be delivered, the relationship with their bank grows stronger and the digital experience gains both relevance and credibility.

3. Self-Management and User Control

Giving customers the ability to decide what, when, and how they receive notifications is essential to avoiding fatigue.

National Australia Bank introduced a control panel in its app to configure preferences, reducing complaints about overload by 25%.

Revolut allows European customers to mute certain temporary alerts (e.g., promotions) while keeping critical ones active (e.g., security).

BAC Credomatic (Central America), with the support of our solution, added a preference center in both Mobile and Online Banking. This allows customers to enable or disable notifications for offers, sales, or security alerts, as well as choose their preferred delivery channel (app or SMS).

Self-management strengthens the perception of respect and builds greater trust in the channel.

4. Gamification and Incentives for Meaningful Engagement

Turning notifications into a positive experience not only captures attention but also strengthens habits and loyalty, making the digital channel both useful and engaging.

Monzo (UK) uses a gamified version of its “Savings Pots,” turning saving into a visual and emotional experience. Users can personalize their goals with images and track a progress bar that fills up with every contribution.

In Brazil, neobanks are adopting gamification to boost customer retention. Some, for example, have launched “Loop”-style programs where users earn points within the app that can later be redeemed for benefits, according to reports in specialized media.

In Latin America, studies such as Mastercard’s 2025 report highlight gamification as a powerful tool for financial inclusion and education. It has proven especially effective in fast-growing markets, where it helps encourage the adoption of healthy financial habits.

5. Omnichannel Integration: Consistency Across the Digital Ecosystem

Effective orchestration prevents redundancy and strengthens message consistency, ensuring each communication reaches customers through the most appropriate channel.

Santander (Spain and Latin America) allows customers to configure alerts from their “Personal” area in online or mobile banking, choosing whether to receive them by email, SMS, or push. They can also set filters, such as minimum amounts required to trigger notifications.

Lloyds Banking Group (UK) has developed an advanced omnichannel strategy where the experience flows seamlessly across app, web, email, and SMS, avoiding duplication. This allows, for instance, an action started in the app to be followed up with updates via the most suitable channel.

Banorte (Mexico), a Latinia client since 2025, offers the option to activate alerts for specific transactions through its digital platform (web and app), sending them both by email and mobile phone to ensure customers receive notifications through the most convenient channel.

6. Transparency, Guidance, and Financial Education

Explaining the value of each notification reduces the sense of intrusion and strengthens customer trust.

ING Netherlands offers an onboarding process in its app that explains the purpose of push notifications, helping users set up the ones most relevant to them.

Ally Bank (U.S.) allows customers to customize alerts for payments, transfers, and security, reinforcing their sense of financial control.

Banco Popular (Costa Rica), in partnership with Visa, provides access to a full financial education platform integrated into its app, which also includes educational notifications and tips to improve users’ financial health.

Beyond operations, notifications become a tool for financial education that strengthens the long-term bank-customer relationship.

Regulation, Trust, and Added Value for the Push Channel

Regulatory frameworks such as DORA, GDPR in Europe, or Mexico’s Federal Law on the Protection of Personal Data require financial institutions to obtain explicit consent and ensure the responsible use of information.

In this context, our approach is built around several key pillars designed to add value and uphold ethical standards in banks’ push notification strategies:

Latinia’s Subscription Engineenables banks to manage opt-ins and opt-outs at a granular level, giving end users the ability to choose which notifications they want to receive, through which channel, and how often. This level of control not only strengthens customer trust but also helps banks meet regulatory requirements without sacrificing communication agility.

Latinia’s NBA Engine leverages real-time data analysis to identify the most relevant and timely actions or messages for each customer. By analyzing customer transactions and interactions as they occur, the NBA engine can predict needs and preferences, delivering personalized notifications that are more likely to engage customers. This personalized approach ensures clients receive relevant alerts and updates, boosting overall satisfaction and loyalty.

Latinia’s Critical Events Gateway ensures critical notifications—such as fraud alerts and transaction confirmations—are delivered reliably across multiple channels, including SMS, push notifications, email, and WhatsApp. The gateway supports automatic reconnection and redirection to guarantee messages are delivered even if the initial attempt fails. This reliability is essential for maintaining customer trust and security, ensuring important alerts are received promptly.

The Near Future: Predictive Personalization and Interactive Omnichannel

The initial question raised a dilemma facing all digital banking today: how to keep notifications relevant without overwhelming users already saturated with constant alerts on their devices. The answer isn’t to limit communication to the bare minimum, but to evolve how notifications are designed, delivered, and perceived. The real challenge is not how many notifications a customer receives, but whether each one delivers value at the right moment.

Technology provides the essential building blocks:

Contextualization and artificial intelligence: timely, relevant messages

User self-management and control

Gamification and incentives for meaningful engagement

Omnichannel integration: consistency across the digital ecosystem

Transparency, guidance, and financial education

However, these tools only reach their full potential when framed within a broader strategy that combines innovation with long-term vision.

Such a strategy requires ethical channel management: notifications aligned with user preferences, transparency about their purpose, and a clear consent model that builds trust. But it also demands an unavoidable human factor—actively listening to customers, understanding what they expect from their bank, and designing communications that feel like a useful, protective service rather than an intrusion.

Within this delicate balance of technology, regulation, and customer experience lies the key to shifting from overload to true relevance. Banks that succeed will ensure every notification is seen not as just another screen interruption, but as a gesture of care and support. In doing so, they will strengthen the three pillars that sustain customer relationships in the digital era: loyalty, security, and satisfaction.

According to Reuters, 43% of users turn off alerts because they find them excessive or irrelevant. The rapid pace of digitalization has made push notifications a cornerstone of communication between…

According to Reuters, 43% of users turn off alerts because they find them excessive or irrelevant. The rapid pace of digitalization has made push notifications a cornerstone of communication between…

According to Reuters, 43% of users turn off alerts because they find them excessive or irrelevant. The rapid pace of digitalization has made push notifications a cornerstone of communication between…

According to Reuters, 43% of users turn off alerts because they find them excessive or irrelevant. The rapid pace of digitalization has made push notifications a cornerstone of communication between…

According to Reuters, 43% of users turn off alerts because they find them excessive or irrelevant. The rapid pace of digitalization has made push notifications a cornerstone of communication between…

According to Reuters, 43% of users turn off alerts because they find them excessive or irrelevant. The rapid pace of digitalization has made push notifications a cornerstone of communication between…

According to Reuters, 43% of users turn off alerts because they find them excessive or irrelevant. The rapid pace of digitalization has made push notifications a cornerstone of communication between…

According to Reuters, 43% of users turn off alerts because they find them excessive or irrelevant. The rapid pace of digitalization has made push notifications a cornerstone of communication between…

According to Reuters, 43% of users turn off alerts because they find them excessive or irrelevant. The rapid pace of digitalization has made push notifications a cornerstone of communication between…

According to Reuters, 43% of users turn off alerts because they find them excessive or irrelevant. The rapid pace of digitalization has made push notifications a cornerstone of communication between…

According to Reuters, 43% of users turn off alerts because they find them excessive or irrelevant. The rapid pace of digitalization has made push notifications a cornerstone of communication between…

Para ofrecer las mejores experiencias, utilizamos tecnologías como las cookies para almacenar y/o acceder a la información del dispositivo. El consentimiento de estas tecnologías nos permitirá procesar datos como el comportamiento de navegación o las identificaciones únicas en este sitio. No consentir o retirar el consentimiento, puede afectar negativamente a ciertas características y funciones.

Funcional

Always active

El almacenamiento o acceso técnico es estrictamente necesario para el propósito legítimo de permitir el uso de un servicio específico explícitamente solicitado por el abonado o usuario, o con el único propósito de llevar a cabo la transmisión de una comunicación a través de una red de comunicaciones electrónicas.

Preferencias

El almacenamiento o acceso técnico es necesario para la finalidad legítima de almacenar preferencias no solicitadas por el abonado o usuario.

Estadísticas

El almacenamiento o acceso técnico que es utilizado exclusivamente con fines estadísticos.El almacenamiento o acceso técnico que se utiliza exclusivamente con fines estadísticos anónimos. Sin un requerimiento, el cumplimiento voluntario por parte de tu proveedor de servicios de Internet, o los registros adicionales de un tercero, la información almacenada o recuperada sólo para este propósito no se puede utilizar para identificarte.

Marketing

El almacenamiento o acceso técnico es necesario para crear perfiles de usuario para enviar publicidad, o para rastrear al usuario en una web o en varias web con fines de marketing similares.