Partner Programs in banking: From vendor to competitive advantage

Latinia

•20 de January de 2026•6 min read

For years, banking operated in a relatively stable environment: innovation cycles were long, competition was clearly defined, and technological progress moved at a manageable pace. Over the last decade, that balance has broken down.

Today, institutions operate in a landscape shaped by global digital platforms and an increasingly distributed value chain.

This shows that structured collaboration is not a secondary option, but a key operational lever to compete.

Our new article explores how Partner Programs are shifting from an operational resource to a strategic lever to accelerate capabilities, reduce risk, and compete in a more distributed market.

At a time when almost every institution collaborates with third parties, what sets apart a bank that simply integrates vendors from one that gains a real competitive advantage from its partner ecosystem?

From operational resource to competitive advantage

The transformation does not lie only in adding more vendors, but in how relationships with them are structured. For years, collaboration with third parties was organized around specific projects: one-off integrations, limited services, or targeted solutions. That approach worked while the environment remained stable and the value chain was clearly defined.

This change is driven by three forces that have converged over the last decade:

The competitive pressure from new players: fintechs, neobanks, aggregators, and BigTechs are capturing specific segments of the value chain.

The growing technological complexity: instant payments, digital identity, biometrics, cloud, AI, enriched messaging, open finance…

The demand for speed and personalization: more contextual, more secure, and more immediate services.

In this context, managing vendors as isolated components is no longer enough. Today, banks work with interdependent sets of solutions, and that interdependence requires a framework to prevent it from turning into operational, technical, or regulatory risk.

This is where Partner Programs begin to make sense: not as a catalog of suppliers, but as a mechanism to organize, validate, and connect technological capabilities that must coexist.

To understand their value, it is worth answering a question that is rarely asked:

What is a Partner Program in banking?

A Partner Program in the financial sector is not an affiliation scheme or a purely commercial model. Unlike other industries, where the goal is often to sell more products through commissions, in banking, the purpose is to integrate technological capabilities, ensure compliance, and accelerate innovation without compromising operations.

6 benefits of Partner Programs in banking

Partner Programs are not new, but their role in the financial sector has changed. They used to operate as supporting tools; today they are starting to function as a strategic layer of the banking ecosystem.

These are the 6 most relevant benefits when they are properly structured:

1. Incorporating new capabilities

For a bank, innovation does not always mean developing; it often means absorbing technology.

Digital identity, biometrics, enriched messaging, fraud prevention, or cloud infrastructure are examples of capabilities that a bank can integrate without building them from scratch.

More than 65% of U.S. banks already rely on specialized fintechs to incorporate new capabilities, especially in digital onboarding, payments, and identity, without developing them internally. – Banks and Fintechs Are on the Partnership Track

A program reduces adoption time and prevents internal resources from being spent on capabilities that other players already master.

2. Reducing technological and operational risk

In non-regulated sectors, choosing a vendor can be a matter of price and functionality. In banking, it involves:

compliance with regulations

operational continuity

information security

data sovereignty

compatibility with the banking core

76% of banks believe that technology alliances reduce regulatory and operational risk by relying on providers that have already been validated for financial environments. – Bank Fintech Partnerships

A Partner Program helps standardize evaluation criteria and therefore reduces risk in the selection process. Fewer bets, more informed decisions.

3. Expanding the reach and quality of the technology ecosystem

Banks do not work with isolated solutions; they work with interdependent sets: payments, messaging, onboarding, biometrics, analytics, cloud…

A Partner Program makes it possible to:

map the market

connect providers with each other

complement capabilities

help banks look beyond their immediate perimeter

This creates something valuable: a broader, more interoperable ecosystem that is less dependent on “a single provider for everything”.

4. Accelerating time to market without sacrificing quality

An institution can take 12 to 24 months to evaluate, tender, integrate, and scale a new provider. If competitors achieve this in 6 months, the advantage is lost.

Cases have been documented where collaboration with fintechs reduced time to market by up to 50% in capabilities such as payments and identity, compared to traditional in-house development cycles. – Barclays

A Partner Program shortens that cycle because:

the scouting has already been done

technical validation is already completed

agreements are advanced

integrations are prepared

Innovation stops being a “project” and becomes a continuous flow.

5. Enhancing collective innovation

Fintechs, technology providers, and banks do not innovate in the same areas or at the same speed. That asymmetry, far from being a problem, is an asset.

A well-structured Partner Program allows innovation to flow between these players, connect, and be tested without each party having to manage relationships with all the others separately. The result is an environment where more proofs of concept, more collaboration, and more iterations emerge with less friction.

6. Optimizing costs and avoiding duplication

Traditional banking has historically faced technological duplication: the same service contracted twice by different departments, the same development replicated across different countries, and so on.

A well governed Partner Program makes it possible to:

avoid duplicate developments

concentrate volumes

negotiate better conditions

benefit from cloud agreements

share integrations across countries

reduce the total cost of technology

Studies on banking platforms and digital ecosystems show that partner orchestration reduces the total cost of ownership between 10% and 30% by eliminating duplication and consolidating providers. – PwC

The goal is not only to spend less, but to spend better.

Conclusion

Banking today competes in a landscape where innovation depends as much on what is built internally as on what can be absorbed from the outside. In this context, Partner Programs do not add vendors; they orchestrate capabilities, reduce friction, and distribute risk among players.

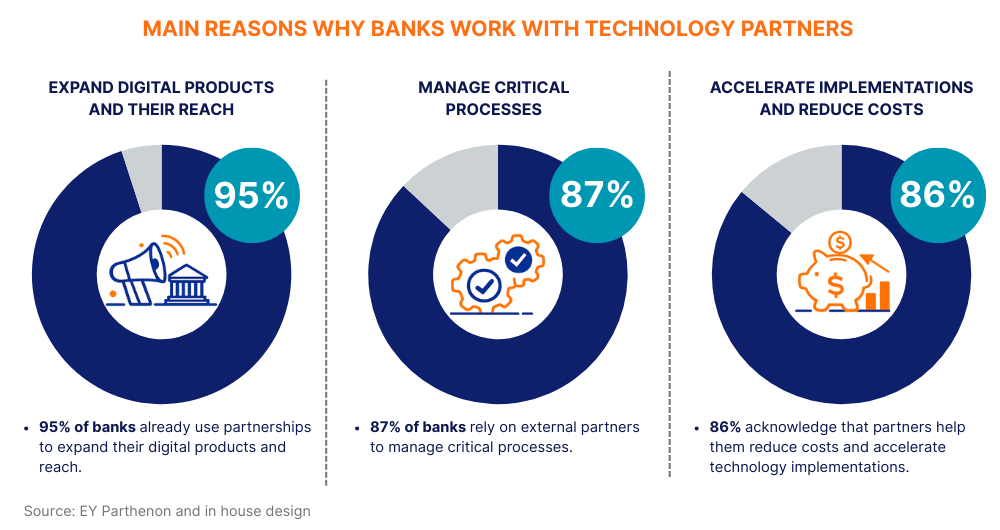

What matters is not that 95% of banks collaborate with third parties —that is already happening— but how that collaboration is governed so it becomes a competitive advantage for banking. This is where Partner Programs become a strategic layer: they accelerate the adoption of new capabilities, reduce selection errors, expand the reach of the ecosystem, enhance collective innovation, and prevent duplication that increases operational costs.

It is an advantage that is difficult to replicate because it does not lie in the technology itself, but in a bank’s ability to adapt it, combine it, and make it coexist with its infrastructure. And as with most complex advantages, few are measuring it; but those who do are beginning to compete differently.

For years, banking operated in a relatively stable environment: innovation cycles were long, competition was clearly defined, and technological progress moved at a manageable pace. Over the last…

For years, banking operated in a relatively stable environment: innovation cycles were long, competition was clearly defined, and technological progress moved at a manageable pace. Over the last…

For years, banking operated in a relatively stable environment: innovation cycles were long, competition was clearly defined, and technological progress moved at a manageable pace. Over the last…

For years, banking operated in a relatively stable environment: innovation cycles were long, competition was clearly defined, and technological progress moved at a manageable pace. Over the last…

For years, banking operated in a relatively stable environment: innovation cycles were long, competition was clearly defined, and technological progress moved at a manageable pace. Over the last…

For years, banking operated in a relatively stable environment: innovation cycles were long, competition was clearly defined, and technological progress moved at a manageable pace. Over the last…

For years, banking operated in a relatively stable environment: innovation cycles were long, competition was clearly defined, and technological progress moved at a manageable pace. Over the last…

For years, banking operated in a relatively stable environment: innovation cycles were long, competition was clearly defined, and technological progress moved at a manageable pace. Over the last…

For years, banking operated in a relatively stable environment: innovation cycles were long, competition was clearly defined, and technological progress moved at a manageable pace. Over the last…

For years, banking operated in a relatively stable environment: innovation cycles were long, competition was clearly defined, and technological progress moved at a manageable pace. Over the last…

For years, banking operated in a relatively stable environment: innovation cycles were long, competition was clearly defined, and technological progress moved at a manageable pace. Over the last…

For years, banking operated in a relatively stable environment: innovation cycles were long, competition was clearly defined, and technological progress moved at a manageable pace. Over the last…

Para ofrecer las mejores experiencias, utilizamos tecnologías como las cookies para almacenar y/o acceder a la información del dispositivo. El consentimiento de estas tecnologías nos permitirá procesar datos como el comportamiento de navegación o las identificaciones únicas en este sitio. No consentir o retirar el consentimiento, puede afectar negativamente a ciertas características y funciones.

Funcional

Always active

El almacenamiento o acceso técnico es estrictamente necesario para el propósito legítimo de permitir el uso de un servicio específico explícitamente solicitado por el abonado o usuario, o con el único propósito de llevar a cabo la transmisión de una comunicación a través de una red de comunicaciones electrónicas.

Preferencias

El almacenamiento o acceso técnico es necesario para la finalidad legítima de almacenar preferencias no solicitadas por el abonado o usuario.

Estadísticas

El almacenamiento o acceso técnico que es utilizado exclusivamente con fines estadísticos.El almacenamiento o acceso técnico que se utiliza exclusivamente con fines estadísticos anónimos. Sin un requerimiento, el cumplimiento voluntario por parte de tu proveedor de servicios de Internet, o los registros adicionales de un tercero, la información almacenada o recuperada sólo para este propósito no se puede utilizar para identificarte.

Marketing

El almacenamiento o acceso técnico es necesario para crear perfiles de usuario para enviar publicidad, o para rastrear al usuario en una web o en varias web con fines de marketing similares.