From Alerts to Value: How the Push Channel Is Evolving in Global Banking (Real-World Case Studies 2025)

Latinia

•10 de October de 2025•6 min read

In today’s digital banking landscape, push notifications are no longer a secondary channel—they’ve become a critical layer of customer interaction. By 2025, the most innovative banks don’t just inform; they anticipate, guide, and enable real-time actions. Push has evolved into a strategic tool that builds trust, drives digital adoption, and strengthens the customer relationship.

How is the banking industry adapting to this shift? Which institutions are leading the transformation—and with what results?

This report explores regional case studies that reveal how push notifications are redefining the banking experience—from conversational personalization in Asia to financial inclusion in Africa, from fraud prevention in Europe to digital activation in Latin America.

Asia: A Laboratory of Sophistication and Engagement

Japón: AI Applied to Automated Savings

In Japan, artificial intelligence has become a key ally for digital banking, powering deeper personalization.

Mizuho Bank, for instance, has launched generative-AI projects to analyze customer behavior and anticipate savings recommendations or automated payments. Though still in a consolidation phase, these systems aim to predict liquidity needs before they arise—reducing friction and strengthening customer trust.

China: Conversational Push in the Superapp Ecosystem

In China’s financial market, superapps such as Alipay dominate the digital experience, transforming push notifications into conversational flows that allow users to pay, invest, or transfer without leaving the chat.

In September 2025, Alipay and Luckin Coffee introduced an end-to-end conversational payment flow—showcasing push’s potential as a gateway to seamless, real-time banking experiences.

Europe: Compliance, Proactivity and Trust under the PSD3

United Kingdom: Adaptive Push Alerts for Fraud Prevention

Amid PSD3’s evolving regulatory landscape, UK banks have placed fraud prevention at the center of their push strategies.

Barclays, for example, is testing adaptive alerts that evolve in real time based on customer behavior, biometrics, and AI-detected spending patterns. When an unusual transaction is detected, the alert doesn’t just inform—it guides the customer through a conversational process to confirm or block the action.

Industry studies suggest these smart systems can reduce false positives in fraud detection by 25–70%, filtering out noise and focusing only on relevant alerts.

Lloyds Bank, meanwhile, has enhanced its digital ecosystem by connecting push notifications with channels like WhatsApp and the web. Through features like Link Pay, customers can receive alerts and complete actions without leaving their preferred environment—cementing push as a key element of a truly omnichannel experience.

Spain and Germany: Contextual Push for Preapproved Loans and Financial Inclusion

Some banks are moving toward more sophisticated personalization by using contextual push notifications.

Deutsche Bank’s Transaction Notification API enables clients to subscribe to real-time alerts for incoming and outgoing transactions, configuring custom rules according to their needs. This infrastructure illustrates how German banks are moving toward automated, contextual communication—where push becomes an active interaction channel rather than a passive notice.

In Spain, CaixaBank continues expanding its use of push within its digital ecosystem—especially for security, financial control, and mobile experience—positioning it as an essential touchpoint in customer engagement.

America: Hyper-Personalization and Real-Time Experiences

United States: Geolocation and Embedded Banking

Banks like Chase and Wells Fargo leverage geolocation and analytics to send personalized alerts or promotions when customers are near merchants or points of interest.

These experiences embody embedded banking—integrating financial services into everyday digital experiences such as shopping, mobility, or entertainment apps—boosting loyalty and engagement without friction.

Latin America: Push for Digital Activation and Transactional Security

Across Latin America, push notifications have become an operational pillar of the mobile banking experience.

Banco de Bogotá integrates a push challenge in its Business App, allowing corporate approvals directly from the phone—enhancing real-time security and control.

Meanwhile, Santander México uses push notifications within its SuperMóvil app not only for alerts but also for guided activations—inviting users to complete transactions or access offers.

These flows strengthen adoption and trust in digital channels, turning everyday operations into seamless, mobile-first experiences.

Africa: Push as a Driver of Inclusion and Mobile Growth

Nigeria: Push as a Pillar of Mobile Banking

In Nigeria, digital banks such as Kudause push notifications as their primary channel for transaction and security alerts—while also integrating microloans and airtime top-ups. This ecosystem accelerates mobile adoption and supports national inclusion goals.

South Africa: From Transactional Push to Digital Stokvel

In South Africa, FNB propels collaborative saving with Stokvel Account, a group account designed for community funds (stokvels) that centralizes everything in the digital channel. Members can check balances and movements via the FNB App, web banking or USSD (cellphone banking), and payments require multiple approvals (multi-signature model) to reinforce internal control.

The bank sends real-time notifications for every deposit or withdrawal in the fund: the inContact / Smart inContact ecosystem allows alerts via app (push) or SMS, providing immediate and shared traceability of each movement. The result is more transparent governance and a cashless operation that reduces common frictions in collaborative saving.

Oceania: Purpose-Driven Banking and Financial Wellbeing

Australia: Sustainability and Wellbeing in the App

Australian banks are redefining push as a tool for purposeful financial guidance. Beyond transactional alerts, apps like CommBankand Westpac now send personalized reminders promoting sustainability and healthier financial habits. Partnering with Cogo, customers can view their estimated carbon footprint and receive timely push notifications that encourage more responsible spending.

New Zealand: Education and Cyber-Safety via Push

Facing rising cyber threats, Kiwibank has evolved its push strategy into a digital sentinel: alerts now notify users of phishing attempts, offer cybersecurity tips, and inform about changes in authentication settings—all within a secure, biometrics-based environment.

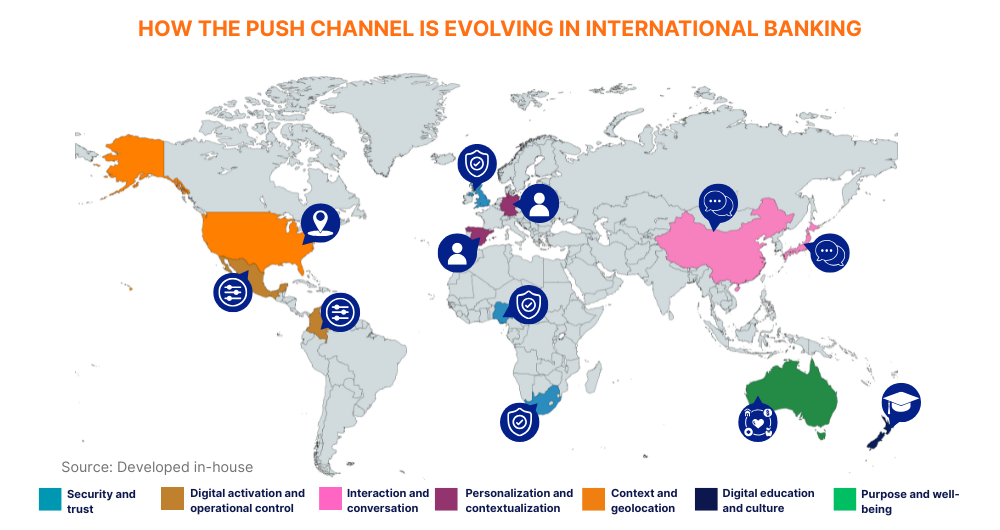

Push Evolves as a Global Response and a Lever for Local Value

In 2025, the banking industry is redefining its relationship with the push channel — transforming it from an informational tool into a strategic layer that combines real-time data, empathy, and consent. This evolution is unfolding across multiple fronts: from hyper-personalization in the United States and Japan, to fraud prevention in Europe, and financial inclusion in Africa and Latin America.

The most recent examples speak for themselves:

Security and trust: In the United Kingdom, Barclays and Lloyds Bank are advancing adaptive, omnichannel alerts that reduce false positives and strengthen customer protection. In South Africa, FNB uses its inContact ecosystem to provide shared, real-time traceability, while Kuda in Nigeria makes push notifications the cornerstone of secure and inclusive mobile banking.

Context and geolocation: In the United States, Chase and Wells Fargo leverage advanced analytics and geolocation data to deliver personalized, embedded real-time experiences — integrating banking seamlessly into customers’ daily lives.

Interaction and conversation: In China, Alipay and Luckin Coffee have developed conversational push flows that eliminate friction and enhance engagement, while Mizuho Bank in Japan combines generative AI and payment automation to anticipate financial needs before they arise.

Personalization and contextualization: In Germany, Deutsche Bank enables clients to configure personalized rules through its Transaction Notification API, and CaixaBank in Spain continues expanding its use of push for financial control, security, and mobile experience.

Digital activation and operational control: In Latin America, Banco de Bogotá and Santander México push the core of approval, assistance, and digital activation processes, reinforcing adoption and real-time control.

Purpose and wellbeing: In Australia, CommBank integrates push notifications with sustainability and financial well-being objectives, while Westpac uses them to promote responsible spending habits and environmental awareness.

Education and digital culture: In New Zealand, Kiwibank redefines the channel as a digital sentinel, using notifications to strengthen fraud prevention and cybersecurity literacy.

Across all these cases, the goal is not simply to notify, but to create value at the right moment, increase retention, and build stronger customer relationships. The key lies not in sending more notifications, but in sending them better — when there is a genuine need, informed consent, and when the experience becomes more useful, seamless, and personalized.

Push has thus become a cross-cutting driver of value and loyalty in digital banking, tailored to the challenges of each region but united by a common logic: relevance, timeliness, and trust.

In today’s digital banking landscape, push notifications are no longer a secondary channel—they’ve become a critical layer of customer interaction. By 2025, the most innovative banks don’t just…

In today’s digital banking landscape, push notifications are no longer a secondary channel—they’ve become a critical layer of customer interaction. By 2025, the most innovative banks don’t just…

In today’s digital banking landscape, push notifications are no longer a secondary channel—they’ve become a critical layer of customer interaction. By 2025, the most innovative banks don’t just…

In today’s digital banking landscape, push notifications are no longer a secondary channel—they’ve become a critical layer of customer interaction. By 2025, the most innovative banks don’t just…

In today’s digital banking landscape, push notifications are no longer a secondary channel—they’ve become a critical layer of customer interaction. By 2025, the most innovative banks don’t just…

Explore the economic trends shaping the banking sector in 2024. From resilience in the face of economic challenges to adapting to changes in interest rates, discover how technology and sustainability define the financial future.

In today’s digital banking landscape, push notifications are no longer a secondary channel—they’ve become a critical layer of customer interaction. By 2025, the most innovative banks don’t just…

In today’s digital banking landscape, push notifications are no longer a secondary channel—they’ve become a critical layer of customer interaction. By 2025, the most innovative banks don’t just…

In today’s digital banking landscape, push notifications are no longer a secondary channel—they’ve become a critical layer of customer interaction. By 2025, the most innovative banks don’t just…

In today’s digital banking landscape, push notifications are no longer a secondary channel—they’ve become a critical layer of customer interaction. By 2025, the most innovative banks don’t just…

In today’s digital banking landscape, push notifications are no longer a secondary channel—they’ve become a critical layer of customer interaction. By 2025, the most innovative banks don’t just…

In today’s digital banking landscape, push notifications are no longer a secondary channel—they’ve become a critical layer of customer interaction. By 2025, the most innovative banks don’t just…

Para ofrecer las mejores experiencias, utilizamos tecnologías como las cookies para almacenar y/o acceder a la información del dispositivo. El consentimiento de estas tecnologías nos permitirá procesar datos como el comportamiento de navegación o las identificaciones únicas en este sitio. No consentir o retirar el consentimiento, puede afectar negativamente a ciertas características y funciones.

Funcional

Always active

El almacenamiento o acceso técnico es estrictamente necesario para el propósito legítimo de permitir el uso de un servicio específico explícitamente solicitado por el abonado o usuario, o con el único propósito de llevar a cabo la transmisión de una comunicación a través de una red de comunicaciones electrónicas.

Preferencias

El almacenamiento o acceso técnico es necesario para la finalidad legítima de almacenar preferencias no solicitadas por el abonado o usuario.

Estadísticas

El almacenamiento o acceso técnico que es utilizado exclusivamente con fines estadísticos.El almacenamiento o acceso técnico que se utiliza exclusivamente con fines estadísticos anónimos. Sin un requerimiento, el cumplimiento voluntario por parte de tu proveedor de servicios de Internet, o los registros adicionales de un tercero, la información almacenada o recuperada sólo para este propósito no se puede utilizar para identificarte.

Marketing

El almacenamiento o acceso técnico es necesario para crear perfiles de usuario para enviar publicidad, o para rastrear al usuario en una web o en varias web con fines de marketing similares.