Invisible Banking: From Notifications to IoT and Wearables

Latinia

•16 de September de 2025•6 min read

In recent years, push notifications have served as the direct bridge between banks and users in the digital environment. However, the rise of IoT (Internet of Things) and the growth of wearables are redefining the ways and contexts in which institutions interact with their customers.

Will banking be able to keep up with a future where alerts move from mobile phones to watches, vehicles, and connected homes?

The central challenge

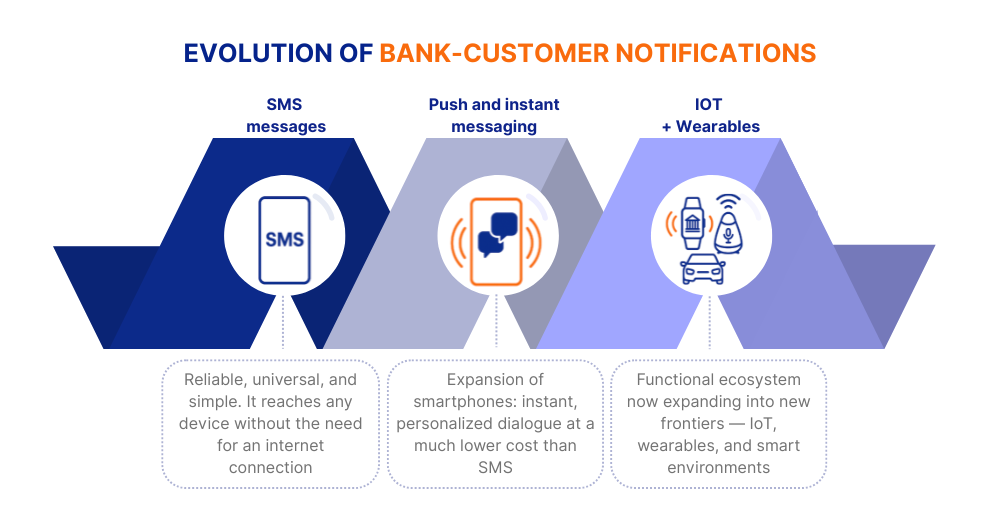

The evolution of notifications: from SMS to the functional ecosystem

Just over a decade ago, SMS was the go-to channel for two-way communication between financial institutions and their customers. It was reliable, universal, and simple. Its strength lay in the fact that it reached any mobile device without needing an internet connection.

With the massive spread of smartphones, push notifications became the new standard. This shift enabled instant, personalized dialogues at a much lower cost than SMS, opening the door to richer interactions and a wide range of key uses: security alerts, account activity notifications, payment reminders, and even personalized offers.

Today, push notifications are a strategic pillar in the bank-customer relationship. Juniper Research estimates that global business messaging traffic will rise from 2 trillion in 2025 to nearly 3 trillion in 2030, driven by the growing need for relevant conversations. This exponential growth presents an unavoidable challenge: avoiding overload and ensuring the relevance of every message.

At the same time, instant messaging —WhatsApp, Messenger, Telegram— has shaped new habits of immediacy and conversation, pushing banks to maintain reliability without sacrificing speed or relevance. Today’s customer expects to receive critical information within seconds, on any device, and in the most convenient format possible.

As a result, push notifications are no longer just occasional alerts on a mobile phone: they have become the operational nexus of digital banking, the entry point to a functional ecosystem now expanding into new frontiers —IoT, wearables, and smart environments— that are reshaping the when, how, and where of financial communication.

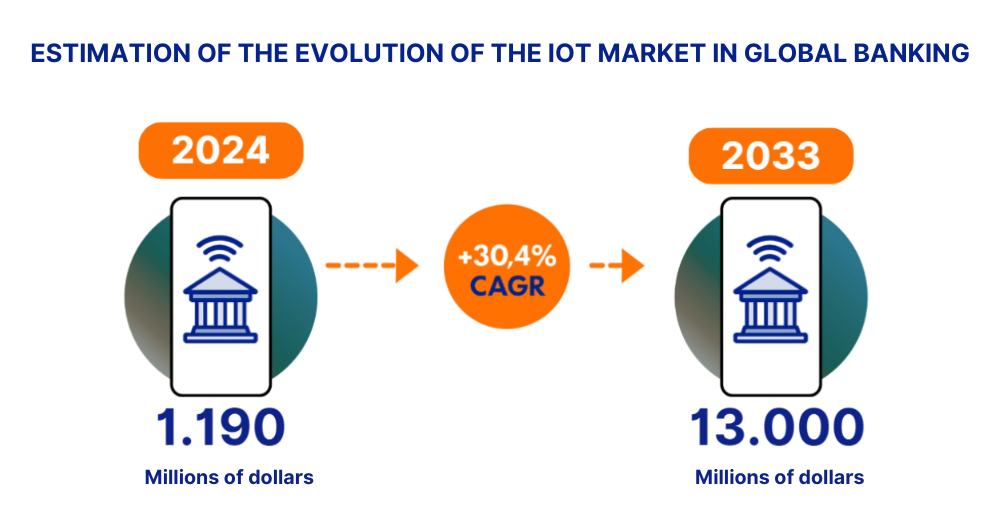

According to Innowise, the IoT market in banking is experiencing rapid momentum: valued at $1.19 billion in 2024, with a projected compound annual growth rate of 30.4%, expected to reach nearly $13 billion by 2033.

Beyond the mobile phone: the rise of connected contexts

The concept of IoT (Internet of Things) refers to the network of physical objects connected to the internet —from household appliances to vehicles, urban sensors, or medical devices— that collect and share data autonomously. Its strength lies in the ability to deliver contextual and continuous interactions, where financial services can be integrated into everyday environments without requiring explicit action from the customer.

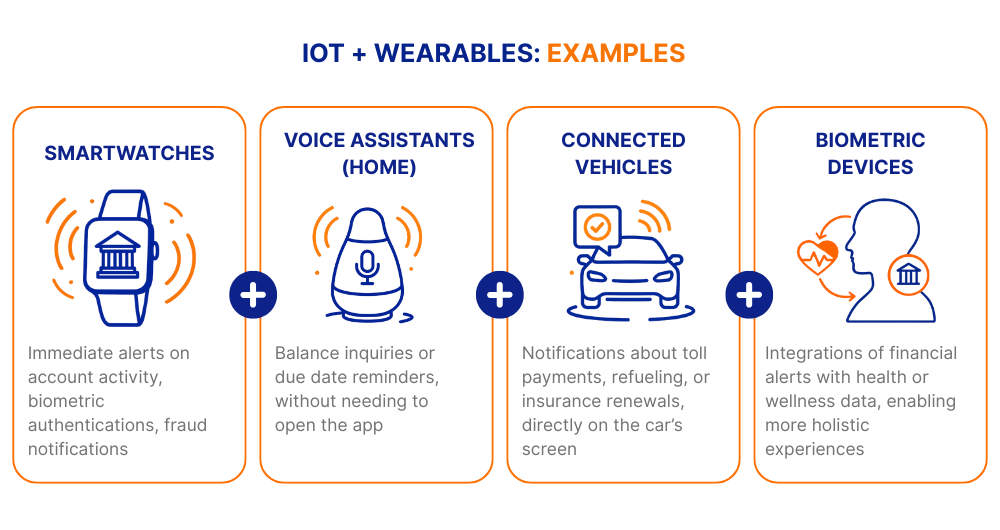

Wearables (wearable technology such as smartwatches, fitness bands, or connected glasses) represent the most personal side of IoT: devices that are always with the user, capable of capturing real-time information about their activity, location, or even health status.

In the banking sector, both phenomena combine to open new possibilities:

This hyper-digitalized environment not only multiplies touchpoints but also changes the logic of notifications: they are no longer isolated interruptions, but part of a ubiquitous ecosystem, always available and adapted to the user’s context.

In 2023, there were approximately 16.6 billion IoT devices connected worldwide, and forecasts indicate that this figure will nearly double to 40 billion by 2030 (IoT Analytics).

Adopting the language of new devices

Adapting banking to wearables is not just about shrinking a mobile notification to fit a smaller screen, but about redesigning the experience based on the device itself. On a smartwatch, for example, the value lies in immediacy and discretion: haptic vibrations to alert about a suspicious charge, simple visual icons to validate a purchase, or quick shortcuts to block a card.

Major players are already setting the course:

Visa and Garmin Pay: an integration that delivers transaction notifications on sports watches, even without a smartphone connection, making purchases on the go easier.

Emirates NBD and Fitbit Pay: Emirates NBD reports that its customers receive instant notifications on their Fitbit device after making a purchase with Fitbit Pay. They can also check their latest transactions from the app linked to the smartwatch.

Mastercard and boAt: Mastercard has partnered with boAt —one of India’s leading wearable brands— to enable tap-and-pay functionality directly from smartwatches. Users can tokenize their Mastercard cards through boAt’s Crest Pay app, allowing fast, secure, contactless transactions without carrying a phone.

This “device language” brings new design codes: short messages, minimal inputs (gesture, tap, voice), and multisensory signals (vibration, icon, light). It’s not just a technological shift but also a communication shift that redefines how banks become present in customers’ daily lives.

Real-life interaction examples: voice and sensing

Voice and sensors are emerging as two key drivers to take banking notifications beyond the mobile phone.

1. Home assistants:

CaixaBank was the first Spanish bank to offer an Alexa Skill with its virtual assistant Neo, allowing customers to make voice inquiries about products, services, and account activity.

Similarly, Capital One was among the first banks in the US to launch an Alexa Skill, providing real-time financial information —such as balances, payments, and transactions— through voice commands. These features work on demand rather than as proactive alerts.

In Asia, a relevant case is YES BANK (India), which has deployed the “YES ROBOT,” a voice and text interface that performs tasks such as transfers, loan inquiries, and payments. Its roadmap also includes integration with Alexa and Google Assistant, pointing to an evolution toward voice banking across multiple devices.

2. Sensing and routines: The integration of IoT allows banking notifications to blend naturally into customers’ daily rhythms, evolving from simple one-off alerts to becoming part of everyday habits. Examples include:

A direct debit alert that automatically appears on the screen of a connected car when it’s started.

Savings reminders or due dates displayed on smart home devices, such as a speaker or even a connected coffee machine.

Contextual alerts linked to biometric wearables, capable of detecting physical activity or stress levels and triggering notifications about unusual spending, credit limits, or real-time financial recommendations.

3. Conversational banking: This type of integration lays the foundation for always-available banking, where notifications not only inform but also enable immediate actions by voice or gesture. Interaction moves beyond a “tap on the phone” to become an experience distributed across the customer’s entire digital ecosystem.

Implications for the customer experience

Toward ubiquitous and proactive banking

Banking communication is no longer one-way. Today, what matters is not just receiving an alert, but receiving it at the right time, through the right channel, and in the right context. Accenture’s 2023 Global Banking Consumer Study highlights that 57% of consumers expect their bank to anticipate needs and deliver personalized communications in real time, marking a clear shift: from “informing” to “anticipating and accompanying.”

In this scenario, wearables play a strategic role. Their portability, physical closeness, and ability to create discreet interactions make them a natural channel for proactive banking. Concrete examples include:

A wrist vibration when a recurring charge is about to hit, giving the customer the chance to validate or manage it before it happens.

A spoken reminder from a voice assistant to renew an expiring card.

An immediate alert on a sports smartwatch after an unusual charge, with the option to confirm or block the transaction directly from the device.

Ubiquity does not mean dispersion, but consistency across every touchpoint: the bank must be present in the customer’s life without intruding, offering useful support at the moments of greatest relevance.

Expectations and frictions: the paradox of hyperconnection

The shift toward omnichannel banking brings an obvious challenge: how to balance personalization with saturation. Customers value receiving contextual and timely information but reject being overwhelmed by irrelevant messages. This tension defines the paradox of hyperconnection: the same infrastructure that enables greater closeness can also erode the experience if not managed wisely.

The question of whether banking is ready for a notification ecosystem beyond the mobile phone cannot be answered without addressing cybersecurity. Every new connected device —a smartwatch, a car, a smart speaker— expands the attack surface. What was once limited to a banking app on a smartphone now extends into much more fragmented and, in many cases, less controlled environments.

Security: from a closed perimeter to a distributed ecosystem

1. Expanded risk: wearables and voice assistants often lack the same security standards as smartphones, making them weak links in the chain.

2. Essential protection:

Multi-factor authentication (MFA)

End-to-end encryption

Biometric validation

At Latinia, we enable banks to establish comprehensive governance of critical notifications, defining dynamic rules about what is sent, through which channel, and under what conditions. Our Critical Events Gateway ensures that sensitive alerts —such as fraud warnings or OTPs— are delivered with priority and traceability, even in case of channel failure. In addition, we integrate with the bank’s existing authentication systems —MFA, native biometrics, or contextual authentication— to strengthen security without adding unnecessary friction. Finally, we guarantee that notifications travel under secure encryption protocols (TLS, HTTPS), protecting end-to-end communication in transit and preserving trust in every interaction.

In Scandinavia, banks like Nordea already allow payments to be approved from a smartwatch using fingerprint or facial recognition, strengthening security without losing usability.

In the United Kingdom, NatWestcarried out a voice banking pilot integrated with Google Assistant, allowing customers to check balances and transactions through secure voice authentication.

In the United States, Midland States Bank launched an Alexa skill that enables customers to check their account balances and transactions by voice. Security is reinforced through a verification PIN that Alexa requests before granting access to information, along with a multifactor authentication process during the initial registration.

Vulnerabilities: the digital periphery as a gateway

In the IoT ecosystem, security is not an add-on but an essential requirement. An outdated firmware, an insecure protocol, or weak credentials can open the door to attacks capable of compromising even the most sensitive notifications, such as a fraud alert or a payment confirmation.

An emerging risk adds to this: the manipulation of push notifications. A cybercriminal could try to mimic a bank’s communication to trick the user into approving a fraudulent transaction. Here, trust depends as much on the content as on the traceability of every message.

We ensure that alerts are always encrypted and controlled, without exposing more sensitive information than necessary.

We enable institutions to apply dynamic validation and prioritization rules, ensuring that each notification originates from a legitimate flow and reaches the customer intact.

We provide real-time monitoring, allowing failures or anomalies to be detected and triggering retries or alternative delivery routes (failover) before the user is left unprotected.

This way, the expansion of notifications to watches, cars, or voice assistants doesn’t have to compromise security or trust. On the contrary, if managed with the right mechanisms, it can consolidate ubiquitous banking as a model that combines convenience and protection, ensuring that digital innovation never strays from its core principle: delivering a service that is secure, reliable, and always available to the customer.

Regulation and emerging standards

The expansion of notifications beyond the mobile phone is also under the regulators’ spotlight. The challenge is no longer only technological but also regulatory and compliance-related, as each new channel introduces additional responsibilities in terms of security and privacy.

Europe: The proposed PSD3 and the Digital Operational Resilience Act (DORA) raise requirements for traceability, strong authentication, and data protection. These regulations are not limited to banking apps but extend to any environment where financial data flows, including IoT devices and wearables. The message is clear: innovation must advance without losing regulatory strength. Regulatory adaptation also includes open finance requirements, which force banks to redesign internal policies and ensure notification traceability in a connected ecosystem.

Latin America: Countries such as Mexico, Brazil, and Chile are moving forward with operational continuity and cyber-resilience regulations, inspired by European frameworks but at varying levels of maturity. While the requirements do not yet reach the same level of detail as in the EU, initiatives are already emerging that push banks to strengthen their architectures to guarantee trust and security.

Global scope: Organizations such as ENISA (European Union Agency for Cybersecurity) warn that wearables and connected devices require specific frameworks for security and authentication when used in financial services. These warnings reinforce the idea that regulation must go beyond banks and include the entire digital ecosystem that is part of the customer relationship.

Future outlook: invisible banking and predictive experiences

Notifications as triggers for advanced services

The progress of IoT points to a future where banking notifications will no longer be simple alerts but triggers for immediate services.

A low balance reminder could automatically initiate a transfer from a savings account with a gesture on a smartwatch; a due date alert could launch a scheduled payment through a voice command in the connected home.

The notification stops being the end of a process and becomes the starting point for an autonomous financial action.

Beyond multichannel: invisible banking

The idea of invisible bankingor ambient finance is gaining traction: interaction with financial services blends into daily life and appears exactly when the customer needs it, without requiring a conscious click. This model relies on predictive algorithms and environmental sensing, capable of anticipating needs and offering proactive solutions.

According to ISG, by 2030 AI agents could manage up to 60% of personal financial life in a silent and transparent way, integrated into wearables, connected cars, and smart home devices.

For banks, moving into this new stage represents both an opportunity and a responsibility. On one hand, it allows them to offer a smoother, more personalized, and higher-value experience; on the other, it requires reinforcing security, traceability, and governance of critical notifications in an increasingly fragmented ecosystem. As Zafin points out, banks that anticipate customer needs and reduce friction in the experience will be the ones to build lasting trust.

The shift from traditional push notifications to a model of predictive and distributed notifications is not optional: it is the condition for banking to remain relevant in a world where digital integrates into every moment of life. The question is not if it will arrive, but which banks will be ready to combine personalization, efficiency, and security without losing customer trust.

In recent years, push notifications have served as the direct bridge between banks and users in the digital environment. However, the rise of IoT (Internet of Things) and the growth of wearables are…

In recent years, push notifications have served as the direct bridge between banks and users in the digital environment. However, the rise of IoT (Internet of Things) and the growth of wearables are…

In recent years, push notifications have served as the direct bridge between banks and users in the digital environment. However, the rise of IoT (Internet of Things) and the growth of wearables are…

In recent years, push notifications have served as the direct bridge between banks and users in the digital environment. However, the rise of IoT (Internet of Things) and the growth of wearables are…

In recent years, push notifications have served as the direct bridge between banks and users in the digital environment. However, the rise of IoT (Internet of Things) and the growth of wearables are…

In recent years, push notifications have served as the direct bridge between banks and users in the digital environment. However, the rise of IoT (Internet of Things) and the growth of wearables are…

In recent years, push notifications have served as the direct bridge between banks and users in the digital environment. However, the rise of IoT (Internet of Things) and the growth of wearables are…

In recent years, push notifications have served as the direct bridge between banks and users in the digital environment. However, the rise of IoT (Internet of Things) and the growth of wearables are…

In recent years, push notifications have served as the direct bridge between banks and users in the digital environment. However, the rise of IoT (Internet of Things) and the growth of wearables are…

In recent years, push notifications have served as the direct bridge between banks and users in the digital environment. However, the rise of IoT (Internet of Things) and the growth of wearables are…

In recent years, push notifications have served as the direct bridge between banks and users in the digital environment. However, the rise of IoT (Internet of Things) and the growth of wearables are…

In recent years, push notifications have served as the direct bridge between banks and users in the digital environment. However, the rise of IoT (Internet of Things) and the growth of wearables are…

Para ofrecer las mejores experiencias, utilizamos tecnologías como las cookies para almacenar y/o acceder a la información del dispositivo. El consentimiento de estas tecnologías nos permitirá procesar datos como el comportamiento de navegación o las identificaciones únicas en este sitio. No consentir o retirar el consentimiento, puede afectar negativamente a ciertas características y funciones.

Funcional

Always active

El almacenamiento o acceso técnico es estrictamente necesario para el propósito legítimo de permitir el uso de un servicio específico explícitamente solicitado por el abonado o usuario, o con el único propósito de llevar a cabo la transmisión de una comunicación a través de una red de comunicaciones electrónicas.

Preferencias

El almacenamiento o acceso técnico es necesario para la finalidad legítima de almacenar preferencias no solicitadas por el abonado o usuario.

Estadísticas

El almacenamiento o acceso técnico que es utilizado exclusivamente con fines estadísticos.El almacenamiento o acceso técnico que se utiliza exclusivamente con fines estadísticos anónimos. Sin un requerimiento, el cumplimiento voluntario por parte de tu proveedor de servicios de Internet, o los registros adicionales de un tercero, la información almacenada o recuperada sólo para este propósito no se puede utilizar para identificarte.

Marketing

El almacenamiento o acceso técnico es necesario para crear perfiles de usuario para enviar publicidad, o para rastrear al usuario en una web o en varias web con fines de marketing similares.